Article by: Carolina Goldstein, Tiago Fernandes, Three Sigma

Compiled by: Frank, Foresight News

Introduction

Tokens play a crucial role in the DeFi ecosystem, but there are differences in achieving protocol goals, value capture mechanisms, and ecosystem integration. Tokens serve as multifunctional tools, including practical tokens for transactions and access, governance tokens for decision-making, or profit-sharing tokens for community wealth distribution. These tokens operate in various environments within DeFi, from decentralized exchanges to lending platforms, and even the underlying infrastructure driving the entire system.

In this article, we will delve into the token mechanisms driving DeFi, from liquidity mining, staking, and voting custody to profit-sharing models, revealing how these mechanisms shape the current landscape of blockchain protocols and how they are adopted by different protocols.

This study includes tokens from the following protocols: 1inch Network, Aave, Abracadabra, alchemx, Angle, Ankr, ApolloX, Astroport, Balancer, Beethoven X, Benqi, Burrow, Camelot, Chainlink, Cream Finance, Compound, Convex Finance, Curve Finance, DeFi Kingdoms, dForce, dYdX, Ellipsis Finance, Euler Finance, Frax Finance, Gains Network, GMX, Hashflow, Hegic, HMX, Hundred Finance, IPOR, Lido, Liquity, Lyra, MakerDAO, Mars Protocol, Moneta DAO (DeFi Franc), MUX Protocol, Notional, Osmosis, Orca, PancakeSwap, Perpetual Protocol, Planet, Platypus Finance, Premia, Prisma Finance, QiDao (Mai Finance), Reflexer, Ribbon Finance, Rocket Pool, Solidly Labs, SpookySwap, StakeDAO, StakeWise, Starlay Finance, SushiSwap, Synapse, Tarot, Tectonic, Thales, Thena, Uniswap, UwU Lend, Velodrome, XDeFi, Yearn Finance, Y2K Finance, Yeti Finance.

It is worth noting that this is not an exhaustive list of DeFi protocol tokens, but a representative selection, with a particular focus on those introducing innovation or slight variations in token mechanisms.

It is worth noting that this is not an exhaustive list of all DeFi tokens, but a representative selection, with a focus on those introducing innovation or slight variations in token mechanisms.

Research Framework

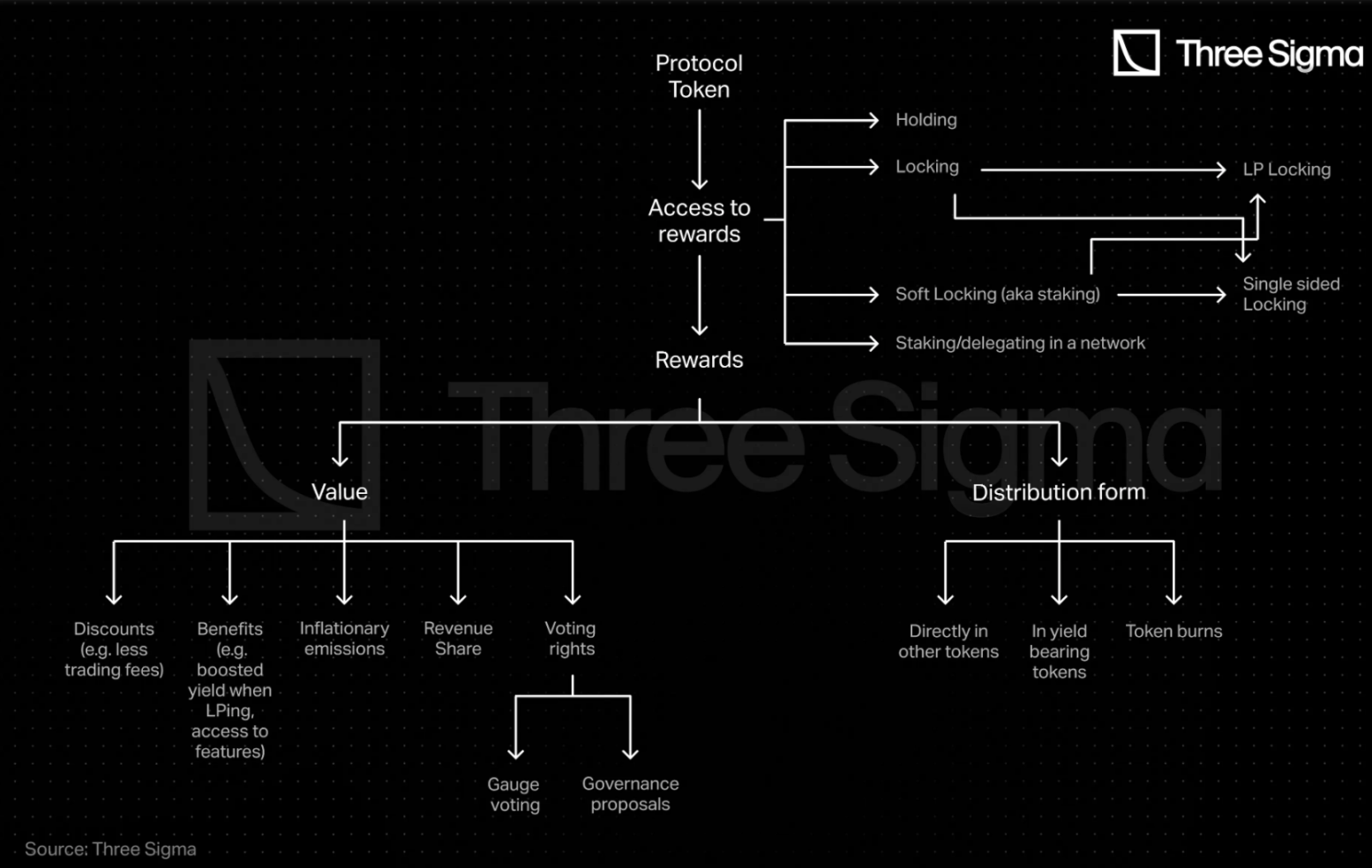

To explore the various roles tokens play in DeFi, we will adopt a systematic approach. After examining over 50 DeFi protocols, a clear common trend emerges: most protocols provide a way for users to earn rewards through their tokens.

The range of these rewards can vary from tangible benefits to more abstract forms of value, potentially including discounts on protocol functions, higher returns for liquidity providers, inflation incentives, a share of protocol revenue, or the ability to vote on key decisions. The distribution of these rewards may also differ, with some tokens being minted or transferred directly, while others may involve the destruction of existing tokens or the generation of income assets.

The ways to earn these rewards also vary: users can earn rewards by simply holding tokens, soft locking, locking, or staking/delegating tokens within the network.

These locking mechanisms may vary significantly across different protocols. Therefore, we will focus on three core aspects to provide a comprehensive understanding of the current token economic landscape: reward access, value, and distribution. It must be recognized that while these options provide pathways for rewarding participation, they should be tailored according to the individual protocol's design and goals.

This article will not use unique terminology for each protocol to describe various token strategies and models, but will use a standardized approach to ensure clarity and ease of comparison. In this article, the following terms will be used:

- Staking: Refers to token staking within the network (for decentralization);

- Locking: Involves locking tokens for a fixed period, with severe penalties for early withdrawal before the lockup period ends.

- Soft Locking: Involves an unspecified lockup period for tokens, with the possibility of unlocking, sometimes incurring withdrawal fees or a waiting period for unlocking, typically referred to as "staking" in typical token economics discussions;

- LP (Soft) Locking: Represents the same concept but specifically related to locking LP tokens;

According to our framework, the protocols included in this article are categorized as follows:

Forms of Reward

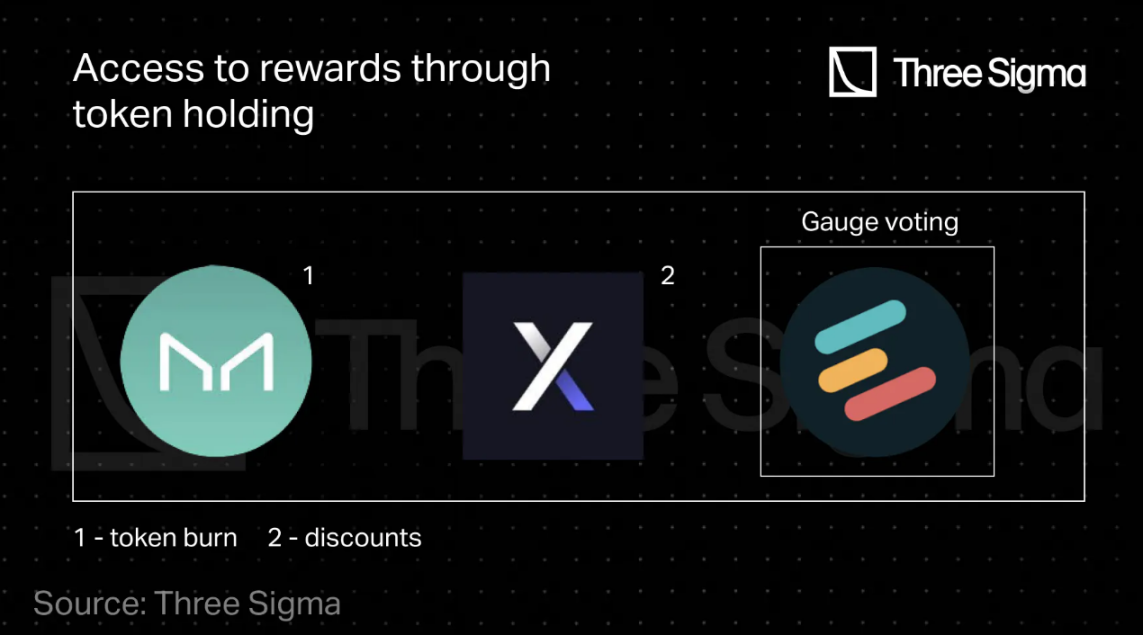

Earning Rewards through Holding

A few platforms, including Euler Finance, MakerDAO, and the recent dYdX, reward users for holding tokens.

dYdX is a prominent derivatives exchange in the DeFi space, and it became a mainstream choice for active traders by offering lower trading fees to DYDX holders.

However, starting from September 29, 2023, dYdX began transitioning all traders to a standard fee structure. Although DYDX primarily serves as a governance tool for the platform, it is worth noting that token holders could previously stake the tokens in a safety module to enhance the protocol's security, but the corresponding fund ceased operations on November 28, 2022.

Euler Finance operates within the DeFi lending track, and holders have the right to influence EUL liquidity incentives and the platform's development direction through delegated governance token EUL. However, users must stake their EUL to participate in voting; holding alone does not yield any direct rewards.

The MKR token of MakerDAO serves a dual purpose. Firstly, MKR holders can actively participate in governance decisions and vote on key parameters. Secondly, in cases of significant market volatility and insufficient collateral value, MKR acts as a protective measure for the protocol—new MKR tokens can be minted and exchanged for DAI in such scenarios.

Although MakerDAO lacks a clear revenue mechanism, MKR holders indirectly benefit from the surplus DAI generated through stability fees, as these surplus DAI can be used to repurchase and burn MRK tokens, reducing the supply.

With the recent launch of the Smart Burn Engine, MKR tokens will accumulate in the form of Uniswap V2 LP tokens instead of being repurchased and burned. Maker will regularly use surplus DAI from the Surplus Buffer to buy MKR tokens from the DAI/MKR liquidity pool on Uniswap V2, and the purchased MKR tokens will then be paired with additional DAI from the Surplus Buffer and provided to the same market. In return, Maker will receive LP tokens and increase the on-chain liquidity of MKR over time.

Some other protocols also adopt a buyback and burn mechanism to indirectly reward token holders, but since most protocols combine this with other mechanisms, they will be mentioned in the later sections of this article.

Earning Network Rewards through Staking or Delegation

Some protocol tokens are rewarded through staking or delegation to achieve network decentralization and enhance ecosystem security. Staking requires token holders to lock their assets as collateral, actively participate in network operations, validation, transaction verification, and maintain blockchain integrity. This aligns the interests of token holders with network security and reliability, providing potential rewards and the risk of losing staked tokens in case of malicious behavior.

Protocols using this staking or delegation mechanism include Mars Protocol, Osmosis, 1inch Network, Ankr, Chainlink, and Rocket Pool.

Osmosis offers multiple staking options for OSMO token holders, including delegating to validators to ensure network security. Delegators receive transaction fee rewards based on the amount of staked OSMO, minus the commission of the selected validator. Stakers (including validators and delegators) receive 25% of newly released OSMO tokens while securing the network.

Additionally, Osmosis offers Superfluid Staking, allowing users to stake tokens in the form of OSMO trading pairs to earn fixed-term (currently 14 days) rewards. These tokens continuously generate swap fees and liquidity mining incentives, while OSMO tokens also earn staking rewards. Osmosis introduced an automated internal liquidity arbitrage mechanism in January this year to accumulate profits, and the community is currently discussing potential uses for these funds, including implementing a burning mechanism that could lead to OSMO deflation.

Mars Protocol, part of the Cosmos ecosystem, operates similarly, allowing token holders to play a crucial role in securing the Mars Hub network, managing outposts, and setting risk parameters through staking or delegation.

The 1INCH token is the governance and utility token of the 1inch Network, primarily used in the Fusion mode, where staked 1INCH is deposited into the "feebank" contract to enable swap transactions. Users delegating 1INCH to support the Fusion mode receive a portion of the generated income. Once staked, tokens cannot be withdrawn until the specified lockup period ends, with penalties for early withdrawal (default lockup period is 2 years). Additionally, 1INCH holders have voting rights in the 1inch DAO, allowing them to influence the platform's development direction.

Ankr's ANKR token has multiple functions, including playing roles in staking, governance, and payments within the ecosystem. A unique aspect of ANKR staking is the ability to delegate to full nodes, not just validators, allowing the community to actively choose reputable node providers. In return, stakers share node rewards and some slashing risk. ANKR staking has expanded to over 18 blockchains, and the ANKR token also supports user participation in governance, including voting on network proposals. Additionally, the ANKR token is used for payments within the network.

Chainlink's native token LINK forms the basis for node operators, allowing individuals to stake LINK and become node operators. Users can also delegate LINK to other node operators, participate in network operations, and share fee rewards. LINK tokens are used for payments within Chainlink's decentralized oracle to support network operations. Additionally, LINK tokens are used to reward node operators providing essential services, including data retrieval, format conversion, off-chain computation, and ensuring normal operation time.

Rocket Pool is a major participant in the Liquidity Staking Derivatives (LSD) space, introducing the RPL token to provide insurance for network slashing risk, enhancing security without the 32 ETH requirement for Ethereum PoS participation. "Minipools" only require 8 or 16 ETH as collateral, with the remaining borrowed from the staking pool. RPL acts as additional insurance, reducing slashing risk. RPL token holders also have governance rights, and the RPL token is used for protocol fee payments, providing a comprehensive toolkit within the Rocket Pool ecosystem.

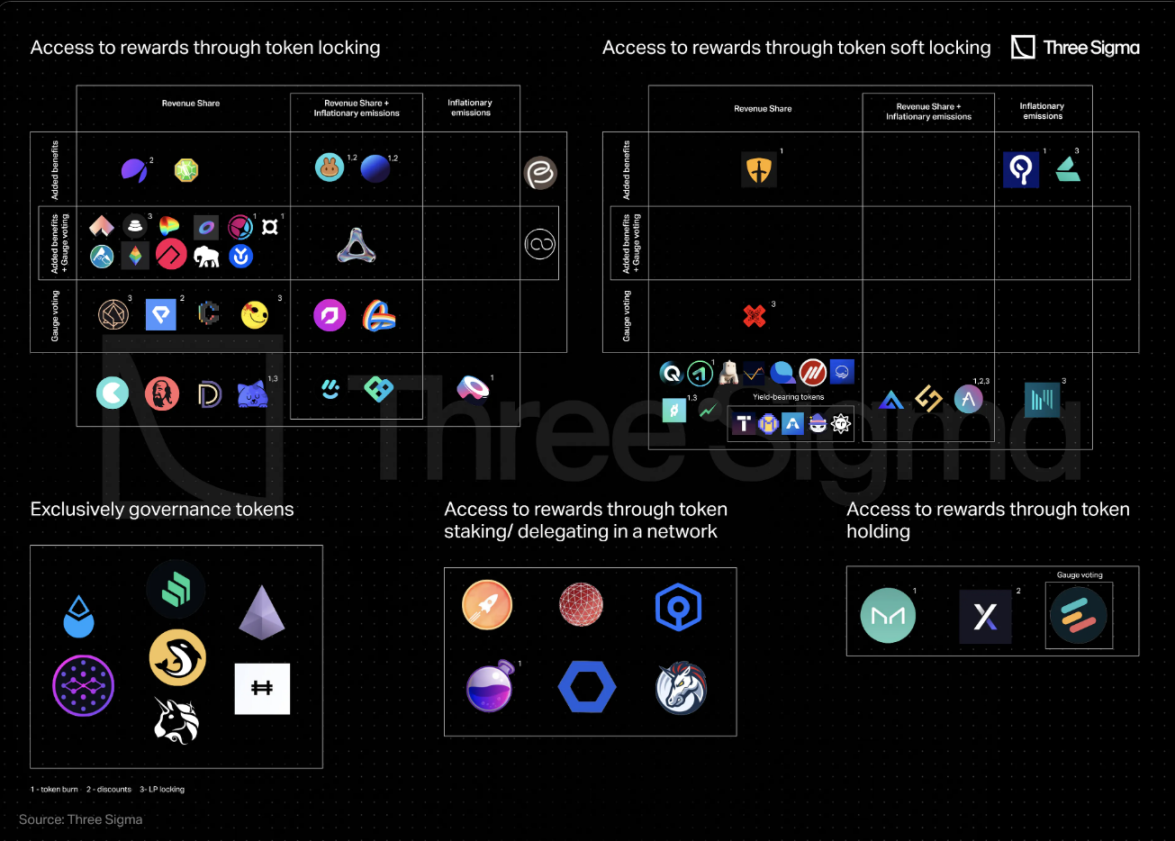

Earning Rewards through Locking

Token locking is a core mechanism for earning protocol rewards in the current DeFi landscape, including profit-sharing, increasing annualized rates, and inflation emissions. Locking primarily takes two forms:

- Single-sided locking: Users lock native protocol tokens;

- LP locking: Users provide liquidity, typically composed of protocol tokens and native network tokens, and then lock LP tokens;

The key to this mechanism is choosing the lockup interval, where users are constrained within that interval until it expires. Some platforms offer options to extend the lockup period for higher rewards, while others allow early unlocking but at a high cost in rewards, making it a strategic decision to balance risk and reward.

Extending the lockup period generates more rewards, such as enhanced voting rights and increased share of protocol revenue, related to commitment and risk reduction factors: a longer lockup period signifies confidence in the protocol, and the protocol rewards with greater incentives in return.

A widely used token locking method is the Vote Escrow model, pioneered by Curve Finance, where users receive veTokens when they lock their governance tokens, granting voting rights but typically being non-transferable. While Vote Escrow solutions are increasingly popular in DeFi platforms, many issues limiting their effectiveness have emerged, including the risk of centralization, where a few large holders gain governance control, as seen in the Curve Wars.

Therefore, more platforms and protocols are improving the concept of Vote Escrow to increase participation and adjust incentive measures for the entire ecosystem. While veTokens are typically non-transferable, some protocols allow the tokens to be used for unlocking liquidity or gaining additional rewards. Many DAOs now use Vote Escrow solutions to manage user participation and rewards.

In Curve DAO, users lock their CRV tokens to gain voting rights, with longer lockup periods resulting in greater voting power. veCRV is non-transferable and can only be obtained by locking CRV, with a maximum lockup period of four years. Initially, one locked CRV for four years equals one veCRV. As the remaining unlock time shortens, the veCRV balance linearly decreases.

As mentioned earlier, this model has sparked conflicts over voting rights, especially in terms of liquidity. Convex has led this conflict, requiring users to lock CVX tokens for at least 16 weeks to vote on Convex proposals, and these tokens will be inaccessible until then.

The Curve fork project Ellipsis Finance on the BNB Chain also follows this model. EPX holders can lock their EPX for 1 to 52 weeks, with longer lockup periods resulting in more vlEPX.

Hundred Finance has ceased operations due to a protocol hack. It adopted a voting escrow model similar to Curve, where locking 1 HND for 4 years generates approximately 1 mveHND, and this balance decreases over time.

Perpetual Protocol, a perpetual contract trading platform, also adopts this model. Users locking PERP into vePERP can increase their governance voting power by up to 4 times.

Many DeFi protocols have embraced derivatives of the voting escrow mechanism to incentivize user participation. Burrow uses a model similar to Curve's ve-token, offering BRRR holders the opportunity to participate in the BRRR locking program. Starlay Finance on Polkadot and several on-chain Cream Finance have introduced similar concepts, allowing token holders to lock LAY and CREAM to receive veLAY and iceCREAM tokens, respectively. Frax Finance also uses this model, where veFXS tokens grant governance voting rights.

Similarly, QiDao and Angle have implemented token locking to gain governance influence. In the options space, Premia and Ribbon Finance offer vxPREMIA and veRBN tokens, respectively. StakeDAO, Yearn Finance, MUX Protocol, ApolloX, PancakeSwap, Planet, SushiSwap, Prisma Finance, and DeFi Kingdoms have also integrated variants of the voting escrow mechanism.

These protocols differ in their reward distribution and benefits provided to users, which we will further explore in this article. Additionally, Solidly Labs, Velodrome, and Thena are notable decentralized exchanges that have evolved from the basis of Curve's voting escrow mechanism, incorporating unique adjustments in their incentive structures through the ve(3,3) mechanism.

Balancer introduces an interesting variation to the Curve model by not directly locking protocol liquidity mining reward tokens, but locking LP tokens. Therefore, users do not need to lock BAL, but they must lock the liquidity tokens BPT used to add to the BAL/WETH 80/20 pool to receive veBAL.

Alchemix also adopts a variant of the LP locking type in the voting escrow model—users can mint veALCX by staking 80% ALCX/20% ETH Balancer liquidity pool tokens.

The Y2K token is a utility token in the Y2K Finance ecosystem, and locking it as vlY2K provides various benefits. Notably, vlY2K is represented in the form of locked Y2K/wETH 80/20 BPT.

Finally, UwU Lend has launched a new lending network built on its own UWU token—by combining UWU with ETH and providing liquidity on SushiSwap, customers can receive UWU-ETH LP tokens, which can be locked for 8 weeks in the DApp.

A key feature in token locking is the commitment to provide higher rewards, such as voting rights, as the lockup period lengthens. This encourages longer lockup commitments and greater influence on protocol decisions. The distinguishing factor among protocols is the maximum lockup period, ranging from a few months to four years. Managing veTokens also varies; some use a linear decay model, gradually reducing voting power, as seen in Curve, Perpetual Protocol, Cream, Angle, and Frax, among others. In contrast, some protocols maintain governance influence even after the lockup period ends, such as Premia.

Various protocols, including SushiSwap, Premia, Ribbon, Yearn, ApolloX, DeFi Kingdoms, and Prisma, allow early unlocking of their tokens but impose punitive measures, such as retaining a portion of earned rewards or introducing high fines.

In conclusion, token locking provides users with stronger governance capabilities and other benefits, which we will further explore in this article.

Earning Rewards through Soft Locking

Soft locking, commonly known as staking, introduces a slightly different locking approach for tokens. Unlike traditional token locking, users do not have to adhere to a fixed lockup period and can unlock at any time. Nevertheless, to incentivize users to engage in longer lockups, protocols typically employ strategies such as voting escrow, where rewards increase with the duration of the lockup period and allow for immediate exit.

Some protocols have a waiting period during the unlocking process or implement a vesting schedule to suppress frequent lock-unlock cycles. In some cases, to encourage stable and active user participation while providing flexibility, unlocking fees are introduced.

Benqi Finance, a lending and liquidity staking protocol on Avalanche, follows the voting escrow approach, allocating QI rewards through liquidity mining, which can then be staked for veQI. When staking QI, the veQI balance linearly increases over time, up to 100 times the staked QI. Upon unstaking, all accumulated veQI will be lost. Yeti Finance, an over-collateralized stablecoin protocol, adopts a similar system.

Beethoven X is the first official fork of Balancer V2 on Fantom, now available on Optimism, and follows the same principle of accumulating veTokens, but requires locking BEETS/FTM 80/20 BPTs.

The popular derivatives exchanges GMX, HMX, and Gains Network offer substantial rewards for token stakers, incentivizing them to stake tokens but without introducing a veToken tokenomics model.

Other protocols like Astroport, Abracadabra, Tarot, and SpookySwap allow users to stake tokens in exchange for yield-bearing tokens, which capture value over time and can be used to redeem staked tokens and any accumulated rewards.

Camelot has attempted a different approach, where xGRAIL is a non-transferable escrow governance token that can be obtained by directly soft locking GRAIL, but requires a vesting period before it can be redeemed for GRAIL.

Additionally, protocols such as Liquity, Thales, XDeFi, IPOR, and Moneta DAO use single-sided soft locking as a means to earn protocol rewards.

Similarly, other protocols also adopt LP soft locking. Interestingly, many protocols utilize LP staking mechanisms to incentivize liquidity as a safeguard against protocol insolvency. Aave and Lyra are two protocols that support LP staking and single-sided staking to incentivize liquidity into their safety modules to prevent fund shortages. Users can deposit AAVE/ETH and WETH/LYRA LP tokens, respectively, in exchange for protocol rewards from the insurance pool. These tokenized positions can be redeemed at any time but with a waiting period. On Notional, users soft lock NOTE/WETH Balancer LP tokens to receive sNOTE tokens. NOTE token holders can initiate on-chain voting to extract 50% of the assets stored in the sNOTE pool in case of under-collateralization for system capital replenishment.

Similarly, users on the Reflexer protocol are responsible for maintaining protocol solvency by soft locking FLX/ETH LP tokens on Uniswap v2.

Hegic uses the Stake&Cover model, where staked HEGIC tokens are used to cover the net losses of options/strategies sold by the protocol and earn net profits from all expired options/strategies. Like Aave and Lyra, staking is used not only for sharing rewards but also for providing protection. Participants in the Hegic Stake&Cover (S&C) pool receive 100% of the earned net premium income (or accrued losses), which is proportionally distributed to all stakers, and users can request withdrawals at any time, receiving funds at the end of each 30-day Epoch.

Finally, a few protocols allow users to choose between soft locking and hard locking.

dForce has introduced a hybrid model that combines both soft locking and hard locking, where locking as veDF earns more rewards than soft locking as sDF.

On Platypus Finance, a cross-stablecoin exchange on Avalanche, users can earn vePTP by staking or locking PTP. For every 1 PTP staked, users can earn 0.014 vePTP per hour (linear accumulation), and the maximum amount of vePTP that stakers can earn is 180 times the amount of staked PTP, which takes approximately 18 months. Additionally, the total vePTP amount is determined from the beginning through locking.

Tectonic allows the soft locking of TONIC tokens as xTONIC, with a 10-day waiting period for withdrawals. It is similar to Tarot, but Tectonic allows users to maximize their rewards by locking their xTONIC tokens.

Rewards - Incentives and Benefits for Stakeholders

After exploring the ways to earn DeFi rewards, let's now delve into the various incentives that users receive for holding, locking, or staking tokens. These include fee discounts, increased yields for liquidity providers, exclusive protocol features, revenue sharing, token issuance, and gauge voting rights.

Protocol Fee Discounts

Many platforms offer discounts to users based on their token holdings and activities. For example, Aave borrowers can lower their interest rates by staking AAVE tokens, while Premia users with over 2.5 million vxPREMIA tokens can receive a 60% fee discount. On PancakeSwap, using CAKE tokens for payment can reduce transaction fees by 5%. Planet offers three-tiered yield-boosting discounts by staking GAMMA tokens. HEGIC token holders can enjoy a 30% options contract discount, and staking APX tokens in the ApolloX DAO can reduce transaction fees.

Revenue Sharing

Revenue sharing can be a powerful incentive, and many protocols now allocate a portion of their income to users who stake or lock tokens, aligning their interests with the platform's success and rewarding contributions to network growth.

Most voting escrow protocols share income proportionally with stakeholders. Protocols such as Curve, Convex, Ellipsis, Platypus, PancakeSwap, DeFi Kingdoms, Planet, Prisma, MUX Protocol, Perpetual Protocol, Starlay, Cream, Frax, QiDAO, Angle, ApolloX, UwU Lend, Premia, Ribbon, StakeDAO, Yearn, Balancer, Alchemix, Y2K, dForce, Solidly, Velodrome, and Thena allocate a portion of protocol income. Typically, about 50% of fees flow to shareholders, but governance voting regularly updates these distributions to emphasize the importance of voting rights. Some exceptions in the voting escrow group include Hundred, Burrow, and Sushiswap. Generally, protocol fees are proportionally distributed among stakeholders. However, a few protocols (such as Starlay, Solidly, Velodrome, and Thena) allocate income based on stakeholders' votes for specific gauges.

Regarding soft locking protocols, most include revenue sharing. Protocols using the voting escrow system (such as Beethoven X, Benqi, Yeti, and Platypus) consider the lockup period and token quantity as factors in determining stakeholders' income share.

In contrast, Aave, GMX, Gains, HMX, IPOR, Astroport, Camelot, Abracadabra, Tectonic, Tarot, SpookySwap, Liquity, Moneta DAO, Reflexer, XDeFi, and Hegic only distribute income based on the quantity of staked tokens.

Some protocols, such as Lyra, Thales, and Notional, do not share revenue but reward users through inflation emissions for soft locking and protecting their platforms.

Inflation Emissions

Regarding inflation emissions, many protocols allocate reserved community governance tokens to liquidity providers and active users to incentivize their participation. While most protocols reserve token emissions for LPs, lenders, and farmers, some protocols use them to reward stakeholders.

As mentioned earlier, Lyra, Thales, and Notional opt for inflation emissions instead of revenue sharing, and SushiSwap also discontinued revenue sharing in its tokenomics redesign in January 2023. In some cases, revenue sharing and inflation emissions are both allocated to stakeholders. Protocols implementing the ve(3,3) tokenomics mechanism (such as Solidly, Velodrome, and Thena) follow this approach.

Additionally, Aave, Planet, MUX Protocol, PancakeSwap, and Perpetual Protocol offer emission-based rewards alongside revenue sharing.

Protocols like GMX and HMX also reward stakers through staked GMX and HMX, which require a one-year vesting period to become true GMX or HMX.

Gauge Voting

Voting escrow has led to gauge voting, where smart contracts accept deposits and emit token rewards to depositors. Gauge voting allows stakeholders to influence emission distribution, guiding the allocation of newly minted tokens in the ecosystem. This control over emissions plays a crucial role in shaping the protocol's development and direction.

Many protocols using voting escrow also support gauge voting, including Curve, Convex, Ellipsis, Platypus, Hundred, Starley, Prisma, Frax, Angle, Premia, Ribbon, StakeDAO, Yearn, Balancer, Beethoven X, Alchemix, Y2K, Solidly, Velodrome, and Thena.

In contrast, protocols such as Perpetual Protocol, Burrow, MUX Protocol, and QiDao do not use gauge voting. Additionally, Euler Finance allows EUL holders to determine EUL liquidity incentives without the need to pre-lock tokens, but they need to soft lock tokens in a gauge to exercise their power.

Additional Rewards

Protocols in DeFi often go beyond direct revenue sharing or token emissions to provide users with extra rewards and benefits.

Similar to gauge voting, many protocols following the veToken tokenomics provide increased emissions for users staking liquidity in gauges. Notable examples include Curve Finance, Ellipsis, Platypus, Hundred, Prisma, Frax, Angle, Ribbon, StakeDAO, Yearn, Balancer, Solidly, and Starley.

Some protocols offer higher yields without gauge voting. Burrow increases yields for borrowing and supplying, PancakeSwap enhances liquidity mining yields for LP tokens, Lyra increases treasury rewards for LPs, Thales boosts emissions for active participants, Planet increases LP rewards, and ApolloX increases trading rewards.

Certain protocols take a personalized approach to providing benefits. For example, Camelot offers a plugin system where stakeholders can choose their benefits from options such as shared revenue, increased liquidity farming emissions, or access to the Camelot Launchpad.

DeFi Kingdoms will provide in-game items as a unique advantage, while Osmosis offers superfluid staking (as mentioned earlier, a method of staking LP tokens in the network to simultaneously receive rewards for protecting the ecosystem and providing liquidity).

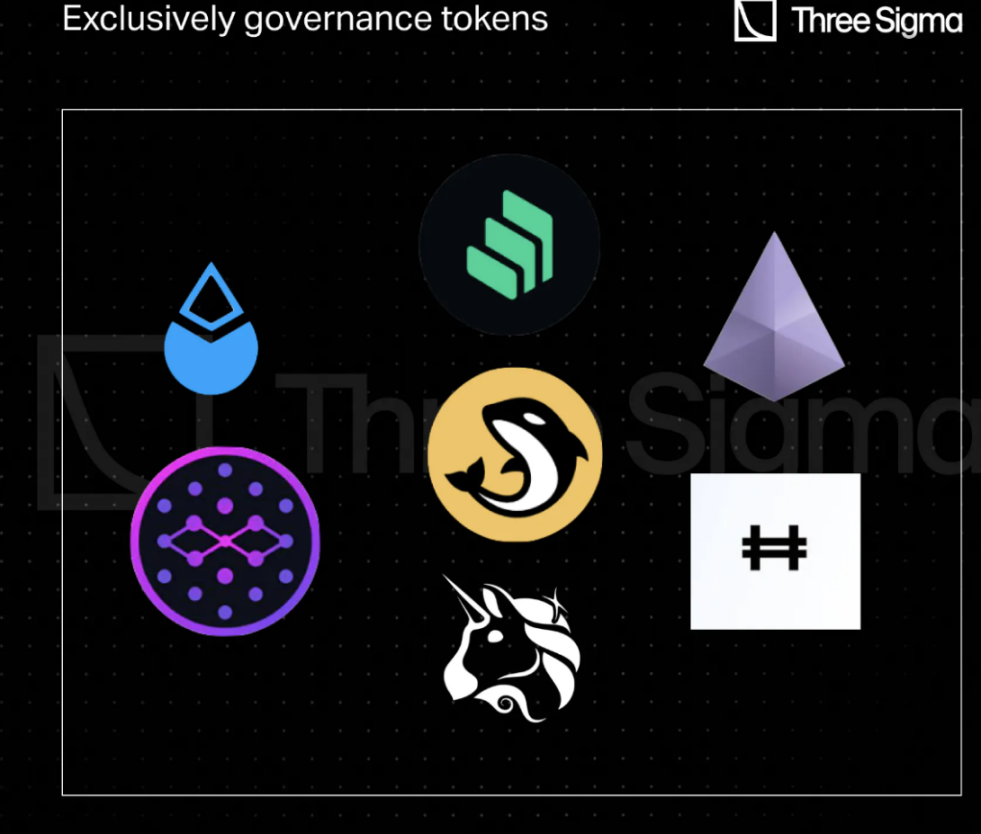

Governance Tokens

In some DeFi protocols, tokens may lack direct utility such as revenue sharing but maintain value through participation in governance. Notable examples include COMP and UNI, whose primary value lies in governance. These tokens enable users to influence the direction of the protocol, where the protocol type seems to play an interesting role, with DEX governance tokens typically being evaluated higher, even with fewer value capture mechanisms, compared to tokens in other categories that hold a smaller proportion of TVL in DeFi. The potential for protocol success, token appreciation, and even promises of future utility are enough to serve as motivation for holding such governance tokens.

LDO is the governance token for Lido, allowing holders to actively participate in decision-making by voting on key protocol parameters to manage the large Lido DAO treasury. Similarly, COMP token holders can vote on governance proposals or delegate their tokens to trusted representatives. UNI token is the governance token for Uniswap, with a market cap of over $30 billion, giving UNI holders the ability to vote, influence governance decisions, manage the UNI community treasury, and determine protocol fees.

Other protocols that do not have specific reward mechanisms built around their tokens include:

- Orca, a decentralized exchange on the Solana network;

- Synapse (SYN), a cross-chain liquidity network effectively integrating 18 different blockchain ecosystems;

- Hashflow (HFT), a gamified DAO and governance platform for participating in cross-chain decentralized exchanges;

- StakeWise (SWISE), a liquidity staking platform primarily focused on decentralized governance, playing a crucial role in the Ethereum ecosystem;

Reward Distribution

Previously, we categorized protocol rewards into five main types: discounts, additional benefits, voting rights, inflation emissions, and protocol revenue sharing. The first three types of rewards are fixedly linked to their distribution methods, while inflation emissions and revenue sharing can take various forms.

Inflation emission rewards mainly take the form of minting governance tokens, such as AAVE, LYRA, and SUSHI, among others. However, some protocols offer inflation emissions in the form of tokens that generate revenue, where the quantity of the original protocol tokens received upon redemption exceeds the initially minted amount.

Examples include Astroport, Abracadabra, Tarot, and SpookySwap, where the value appreciation of tokens generating revenue may stem not only from inflation but also from protocol income. Other protocols distribute income in its original form, such as fees paid in ETH, or many protocols employ a buyback mechanism to repurchase their own tokens from the open market to increase their value and then redistribute them to stakeholders.

Many protocols choose the buyback and redistribution mechanism, including Curve (CRV), Convex (cvxCRV), Perpetual Protocol (USDC), Cream (ycrvlB), Frax (FXS), QiDAO (QI), Angle (sanUSDC), Premia (USDC), Ribbon (ETH), StakeDAO (FRAX3CRV), Yearn (YFI), Balancer (bb-a-USD), Beethoven X (BEETS), Gains (DAI), HMX (USDC), IPOR (IPOR), Abracadabra (MIM), DeFi Kingdoms (JEWEL), PancakeSwap (CAKE), Planet (GAMMA).

Other protocols directly reward stakeholders through token accumulation, such as GMX, Ellipsis, Platypus, Starlay, Solidly, Velodrome, Thena, and Liquity.

Additionally, some protocols implement token burning. They do not redistribute repurchased protocol tokens but instead burn a portion of the tokens to reduce circulating supply, increase scarcity, and hopefully raise the price. By holding the tokens, users indirectly receive protocol income, as the protocol uses accumulated rewards to remove these tokens from circulation.

Some protocols implementing token burning include Aave, Gains, Camelot, Starlay, PancakeSwap, UwU Lend, Planet, MakerDao, Osmosis, SushiSwap, Reflexer, Frax, and Thales.

Conclusion

While the distribution of protocol categories covered in this article may not comprehensively reflect the current state of the entire DeFi landscape, it still provides some key insights.

Specifically, the article mentions 14 lending protocols, 20 DEXs, 5 derivatives protocols, 7 options protocols, 5 Liquidity Staking Derivatives (LSD) protocols, 10 CDP protocols, and 9 other protocols, with analysis also conducted on protocols with similar characteristics but not explicitly mentioned.

Among DEXs, there is a tendency to use locking, especially in the context of voting escrow, while lending and CDP platforms show a preference for soft locking. However, some CDP protocols still use hard locking, and the reason behind this difference may be that, compared to other protocols, DEXs have a greater demand for liquidity, while lending and CDP protocols typically balance between liquidity supply and demand. This is because when there is high demand for loans, there is usually enough supply to meet the demand due to corresponding adjustments in interest rates. In contrast, the primary source of income for DEX liquidity providers is trading fees, and competing with mature DEXs may be challenging.

Therefore, DEXs often use inflation emissions as incentives and manage token supply through locking mechanisms. Generally, soft locking is a more common method in DeFi protocols, but there are notable exceptions among top DEXs. This trend is influenced not only by protocol categories but also by their launch time and reputation. Many leading DEXs today belong to the earliest ones launched, and the decision to lock governance tokens in mature protocols is very different from the decision to lock tokens in newer, usually experimental protocols.

Today, most protocols using locking mechanisms choose to reward users in the form of shared revenue rather than relying on inflation token emissions. This shift represents a significant improvement over the past few years, allowing protocols to consistently incentivize users to act in ways beneficial to the entire community. This is the most explicit way to adjust incentive measures, although the long-term viability is still uncertain due to regulatory considerations.

When it comes to income distribution, token burning is the most commonly used method. From an economic perspective, buyback and redistribution of tokens as needed seems more logical, such as distributing them to token holders who play a more important role in the protocol. However, from a regulatory perspective, buyback and burning of tokens is the simplest way to return protocol income to token holders without making it look like dividend distribution and potentially classifying the tokens as securities. Although this method has been effective for some time, the future of this mechanism is still uncertain. Additionally, some protocols are also heavily influenced by their token economics recognized at the time of listing or token updates. The emphasis on actual earnings and revenue sharing is a mainstream narrative in DeFi, influenced not only by protocols but also by broader market conditions. For example, it is now difficult to imagine a token that requires a four-year lockup being very attractive.

The token model of voting escrow has evolved into the most comprehensive approach, including not only token locking but also voting rights, incentive management, and revenue sharing.

Nevertheless, prominent protocols often grant voting rights through tokens without a clearly defined value capture mechanism. While governance power has significant value, this approach is not feasible for smaller or recently launched protocols, even if these protocols quickly gain adoption and contribute to the DeFi community, whether they can stand the test of time remains the biggest challenge.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。