- Student author: @0x0_chichi

- Supervising teacher: @CryptoScott_ETH

- Initial release date: 2024.5.9

- The revenue sources of the Ethena Protocol are spot collateral yield + funding rate yield from short positions. The introduction of BTC collateral dilutes the collateral yield, and the market's calmness and a large number of Ethena's short positions have reduced the funding rate yield.

- Adding collateral types is a necessary step for the long-term development of Ethena, but it implies the possibility of long-term low interest.

- Currently, the protocol's insurance fund is not sufficient, posing a high risk.

- Ethena has a natural advantage in dealing with runs that occur when facing negative funding rates.

- The total open interest in the market is an important indicator limiting the issuance of USDe stablecoin.

Ethena is a stablecoin protocol built on the Ethereum blockchain, which provides a "synthetic dollar" USDe through the Delta-neutral strategy.

The working principle is as follows: users deposit stETH into the protocol, minting an equivalent amount of USDe. Ethena uses an off-exchange settlement (OES) scheme to map the stETH balance to a CEX as collateral, taking a short position in an equivalent amount of ETH perpetual contracts. This investment portfolio achieves Delta neutrality, meaning that the value of the portfolio does not change with the fluctuation of ETH's price. Therefore, theoretically, USDe achieves price stability.

Users can then pledge the USDe back into the protocol, minting sUSDe, and holding sUSDe can generate income from funding rates. This income once reached over 30%, which was one of the main means for Ethena to attract deposits.

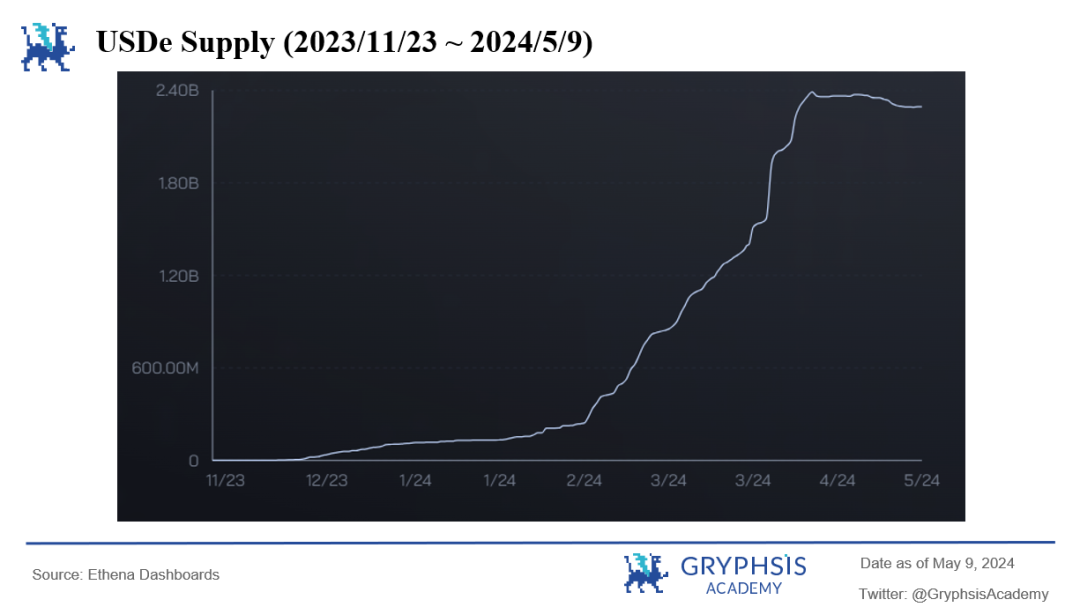

As of May 9, 2024, the yield for holding sUSDe is 15.3%, and the total issuance of USDe has reached 2.29 billion USD, accounting for approximately 1.43% of the total stablecoin market value, ranking fifth.

In the Ethena protocol, both stETH collateral and ETH perpetual contract short positions will generate income (from funding rates). If the combined yield of the two positions is negative, the insurance fund in the Ethena protocol will make up for the loss.

What is the funding rate?

In traditional commodity futures contracts, the parties agree on a delivery date, which is a deadline for physical exchange. Therefore, in the approach of the delivery date of a futures contract, the theoretical futures price will be equal to the spot price. However, in digital currency trading, to reduce delivery costs, the widely adopted form is perpetual contracts: compared to traditional contracts, the delivery process is eliminated, leading to the disappearance of the correlation between futures and spot prices.

To address this issue, the funding rate is introduced, i.e., when the perpetual contract price is higher than the spot price (positive basis), long positions pay the funding rate to short positions (the funding rate is directly proportional to the absolute value of the basis); when the perpetual contract price is lower than the spot price (negative basis), short positions pay the funding rate to long positions.

Therefore, the further the perpetual contract price deviates from the spot price (the larger the absolute value of the basis), the higher the funding rate, and the stronger the suppression force for price deviation. The funding rate becomes the correlation between futures and spot prices in perpetual contracts.

Ethena holds ETH short positions and stETH, and the income comes from funding rates and collateral yield. When the combined yield is positive, the insurance fund will reserve a portion of the income to compensate users when the combined yield is negative.

In the current bull market, the sentiment for long positions is significantly higher than that for short positions, and the demand for long positions in the market is greater than that for short positions, leading to the funding rate remaining at a high level for a long time. The Delta risk of spot collateral in the Ethena protocol is hedged by short positions in perpetual contracts, and holding short positions can generate a large amount of funding rate income, which is the reason why the Ethena protocol generates risk-free high returns.

Before the launch of USDe, the stablecoin project UXD on the Solana chain also stabilized the coin in the same way, but UXD used hedging in DEX contracts, which also laid the groundwork for the failure of UXD.

From a liquidity perspective, centralized exchanges hold over 95% of the share of open interest. To expand the scale of USDe to the billion level, centralized exchanges are the best choice for Ethena: when the issuance of USDe grows on a large scale or when a run occurs, the price of Ethena's short positions will not cause too much disturbance to the market.

Because Ethena uses hedging on centralized exchanges, it will inevitably create new centralized risks. Therefore, Ethena has introduced a new mechanism, OES, which entrusts the collateral to third-party custody (Copper, Fireblocks), and centralized exchanges do not hold any collateral, similar to depositing users' collateral into a multi-signature wallet, maximizing the reduction of centralized risks.

The insurance fund is an important component of the Ethena protocol, transferring a portion of the combined yield of stETH positions and ETH short positions when it is positive to be released when the combined yield is negative, to maintain price stability.

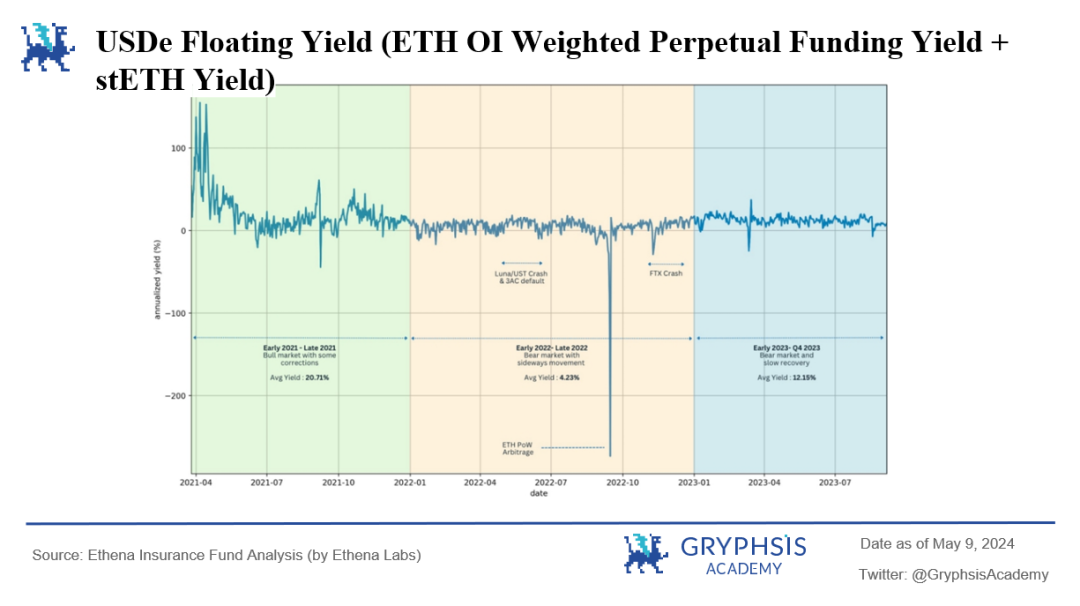

Figure 1: Simulated Floating Yield of USDe

The high USDe yield during the bull market in 2021 reflects strong bullish demand, with long positions having to pay a 40% funding rate to short positions each year. As the bear market began in 2022, the funding rate often fell below zero but did not continue to be negative, and the mean value could still be maintained above 0.

In the second quarter of 2022, the collapse of Luna and 3AC had surprisingly little impact on the funding rate. A brief downturn caused the funding rate to hover around 0 for a period, but it quickly returned to a positive value.

In September 2022, Ethereum's transition from POW to POS triggered the largest black swan event in the history of the funding rate, with the funding rate dropping to 300% at one point. The reason for this was that in this transition, users only needed to hold ETH spot to receive short rewards, leading to a large number of users holding both long positions and short positions in ETH to hedge a large amount of ETH spot.

A large influx of short positions caused the funding rate of ETH perpetual contracts to plummet in a short period of time, but after the end of the short position issuance, the funding rate quickly returned to a positive level.

The collapse of FTX in November 2022 also led to a drop in the funding rate to -30%, but it did not last, and the funding rate quickly returned to a positive value.

Based on historical data calculations, the average combined yield of USDe has always remained above 0, demonstrating the long-term viability of the USDe project. However, short-term normal market fluctuations or black swan events leading to a combined yield less than 0 are unsustainable, and sufficient insurance funds can ensure a smooth transition for the protocol.

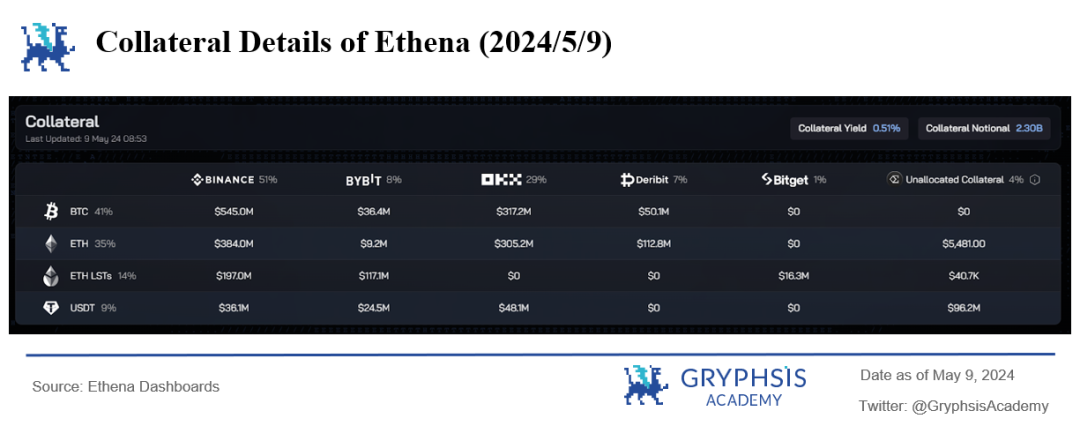

Starting from April 2024, users can collateralize BTC in the Ethena protocol to mint the USDe stablecoin. As of May 9, 2024, the current BTC collateral has accounted for 41% of the total collateral.

Figure 2: Details of Ethena Collateral as of May 9, 2024

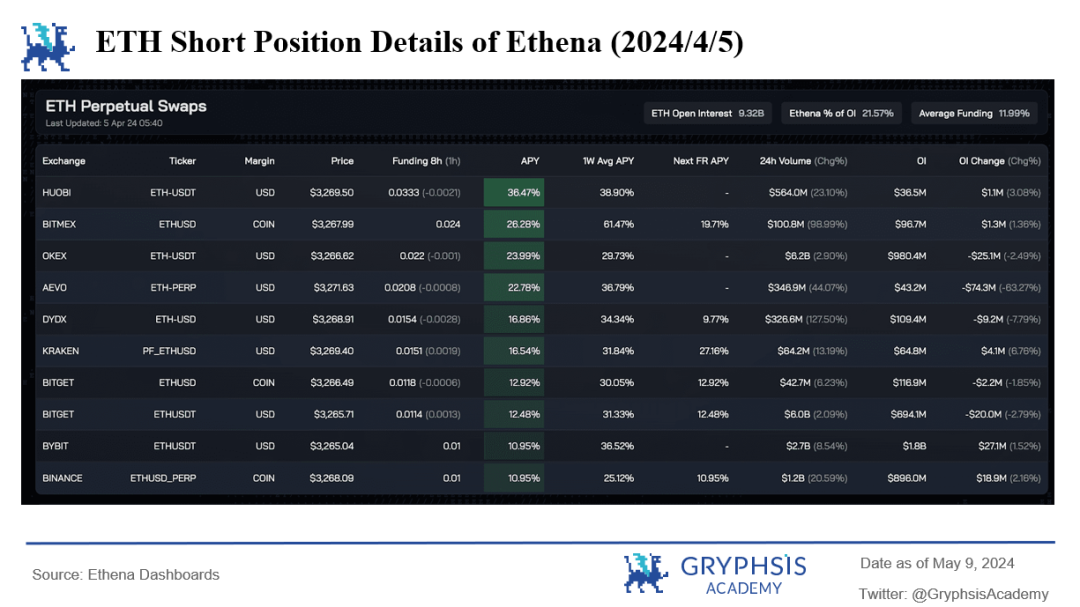

Figure 3: Details of ETH Short Positions in the Ethena Protocol as of April 5, 2024

On the eve of Ethena accepting BTC as collateral, the total amount of ETH short positions in Ethena had already accounted for 21.57% of the total open interest. Despite the strong liquidity of centralized exchanges and Ethena holding ETH short positions on multiple exchanges, the rapid growth of USDe's issuance may lead to insufficient liquidity in ETH perpetual contracts on centralized exchanges. Ethena urgently needs new growth points.

Compared to liquidity collateral tokens, BTC does not have native collateral yield. If BTC is introduced as collateral, the collateral yield contributed by stETH will be diluted. However, the open interest of BTC perpetual contracts in centralized exchanges exceeds 20 billion USD. After introducing BTC collateral, the short-term expansion capability of USDe will increase rapidly. However, in the long term, the growth rate of the total open interest of BTC and ETH perpetual contracts is the main factor limiting the growth of USDe.

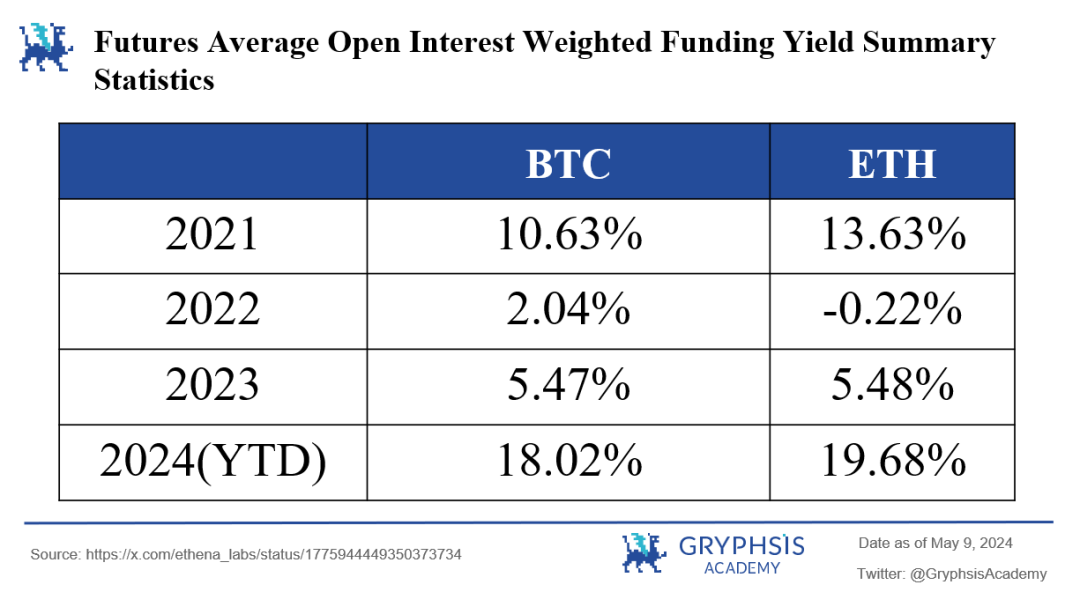

Figure 4: Average Funding Rate Yield for Each Year

Although BTC collateral dilutes the collateral yield of stETH, historical data calculations show that the average funding rate of BTC perpetual contracts is lower than that of ETH in a bull market and higher than that of ETH in a bear market. This is also a hedge against the low funding rate in a bear market, increasing the diversification of the investment portfolio and reducing the risk of USDe deviating from its peg in a bear market.

Currently, the yield of sUSDe has rapidly dropped from over 30% to around 10%, both due to the overall market sentiment and the impact of a large number of short positions resulting from the rapid expansion of USDe.

It is well known that the terrifying growth rate of USDe comes from the super high funding rate payments in a bull market. However, as a stablecoin, USDe still lacks significant use cases, and the existing trading pairs are only associated with some other stablecoins. Therefore, the vast majority of USDe holders hold USDe solely to earn high APY and participate in airdrops.

Although the mechanism of the insurance fund enters into comprehensive negative interest rates, users providing stETH will redeem when the comprehensive yield is lower than the stETH collateral yield. On the other hand, users providing BTC will be more cautious. With the gradual reduction of the basis, the funding rate income continues to be low. Without super high APY, a large amount of redemption may occur after the end of the second round of airdrops. The reason can be compared to the dilemma faced by Bitcoin L2: a large number of users (especially large holders) regard BTC as a target for value storage and have extremely strict requirements for fund security.

Therefore, the author believes that if the stablecoin use case of USDe has not made a breakthrough development before the end of the second quarter airdrop event of Ethena, combined with the gradual reduction of the funding rate, USDe is likely to collapse.

The official Ethena simulation calculation yields the following conclusions about the insurance fund:

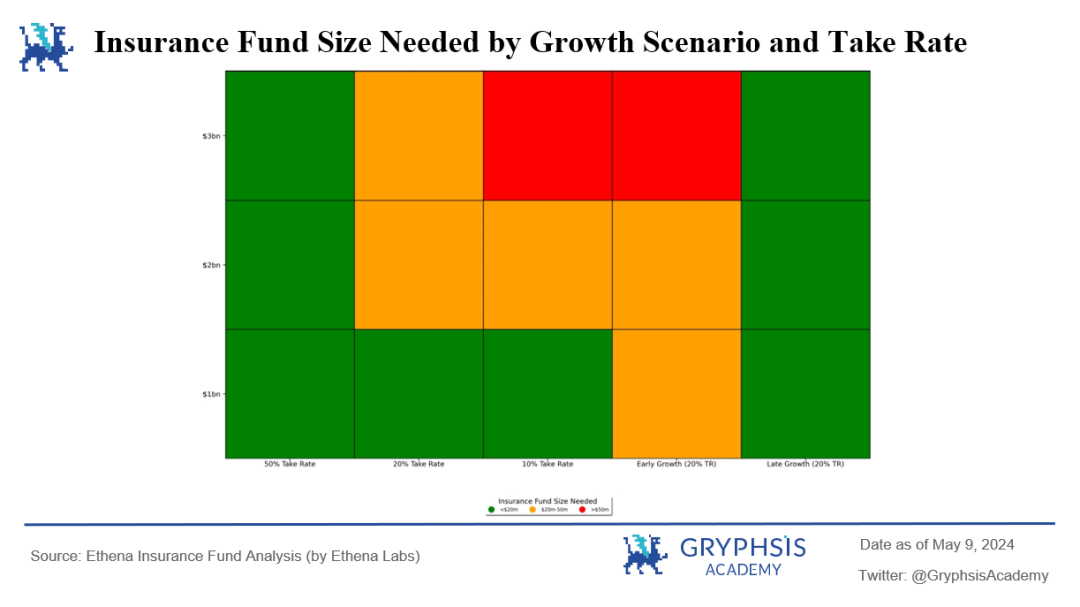

Figure 5: Initial Required Insurance Fund Size by Growth Scenario and Insurance Fund Withdrawal Rate

In Figure 5, green, yellow, and red represent the initial insurance fund size being less than 20 million USD, between 20 million and 50 million USD, and greater than 50 million USD, respectively, to ensure fund security.

The vertical axis represents the expected final issuance amount of USDe within two and a half years (2021/4~2023/10), reaching 1 billion USD, 2 billion USD, and 3 billion USD, respectively. The horizontal axis first three represent when the issuance amount of USDe is linearly increasing, the insurance fund withdrawal rate is set at 50%, 20%, and 10%, respectively. The fourth represents when the issuance amount of USDe remains unchanged after exponential growth in the first year, the insurance fund withdrawal rate is set at 20%. The fifth represents when the issuance amount of USDe continues to grow exponentially, the insurance fund withdrawal rate is set at 20%.

From Figure 5, it can be concluded that for an initial insurance fund of 20 million USD, a 50% withdrawal rate is very safe and can almost always ensure the adequacy of the insurance fund capital under all growth scenarios and levels. If a black swan event occurs before the insurance fund has the opportunity to be capitalized through forward fundraising, early exponential growth may pose a danger to the solvency of the insurance fund. Late-stage exponential growth is safer because it provides more time for the growth of the insurance fund.

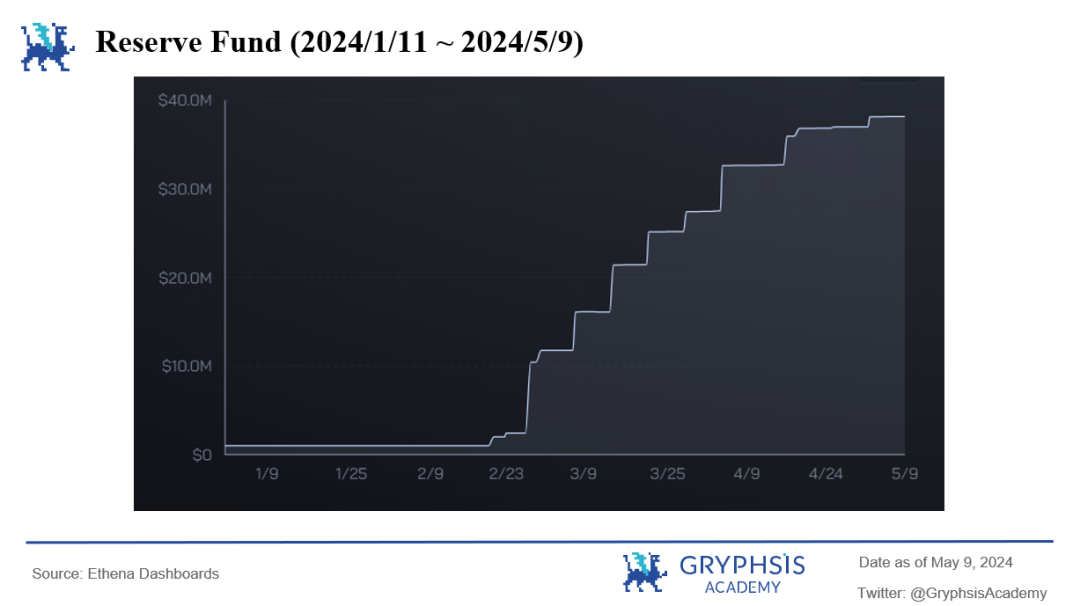

However, the actual situation is that the initial insurance fund is only 10 million USD, and the supply of USDe is growing much faster than the early exponential growth scenario in the model. Currently, in the 38.2 million USD insurance fund (only accounting for 1.66% of the issuance of USDe), nearly half has been added in the last month. It can be seen that the rapid issuance of USDe has led to a severe shortage of the early insurance fund of the Ethena project compared to the official model calculation.

Insufficient insurance funds will have two consequences:

- Users lack confidence in the project, and if high returns start to decline, the project's TVL will gradually decrease.

- With high TVL and low insurance funds, the project must increase the insurance fund withdrawal rate (to at least 30% or higher) as quickly as possible to replenish the insurance fund. However, in the current situation of gradually declining funding rate income, users' yields will be further affected, potentially exacerbating the first consequence.

Figure 6: Total USDe Issuance from November 23, 2023, to May 9, 2024

Figure 7: Insurance Fund Amount from January 11, 2024, to May 9, 2024

Referring to the ETH Pow arbitrage event in the third quarter of 2022 in Figure 1, the funding rate experienced a huge drop in a short period, once exceeding 300% annually. In such black swan events, a run on USDe is almost inevitable, but USDe's unique mechanism seems to have a natural advantage in dealing with runs.

In the early stages of a significant funding rate decline, a run may have already occurred. Due to the run, the Ethena protocol needs to return a large amount of spot collateral and close an equivalent amount of short positions. As the short positions decrease, the expenditure of the insurance fund also decreases, allowing the insurance fund to be maintained for a longer period.

From a liquidity perspective, when a run occurs, Ethena needs to close short positions. In a market with a negative funding rate, this means that long liquidity is exceptionally sufficient, and closing short positions will almost not be troubled by liquidity issues.

At the same time, the 7-day cooling-off period for sUSDe (collateral cannot be liquidated within a week) in the Ethena protocol can also serve as a buffer in the event of a market mutation.

But all of this is contingent on the adequacy of the insurance fund.

The total open interest (OI) in the market has always been a key factor limiting the issuance of USDe and a potential risk for USDe in the future. As of May 9, 2024, ETH OI in the Ethena protocol accounts for 13.77% of the total OI, and BTC OI accounts for 4.71%. The substantial amount of short positions generated by the Ethena protocol has already caused some disturbance in the contract market, and the subsequent expansion of USDe may encounter liquidity issues.

The best solution to this problem is to increase as many high-quality collaterals as possible (with a long-term funding rate greater than 0), which can not only raise the upper limit of USDe supply but also increase the diversification of the portfolio and reduce risk.

In summary, the Ethena protocol demonstrates its unique stablecoin mechanism and sensitive response to market dynamics. Despite facing challenges such as long-term low basis, insufficient insurance funds, and potential run risks, Ethena has maintained its competitiveness through innovative off-chain settlement mechanisms and diversified collateral types.

As the market environment continues to change and technological innovation within the industry progresses, Ethena must continuously optimize its strategies and enhance its risk management capabilities to ensure the adequacy of the insurance fund and the stability of liquidity. For investors and users, understanding the operation mechanism of the protocol, the source of income, and its potential risks is crucial.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。