Original author: David Hoffman

Original translation: Deep Tide TechFlow

The EIGEN airdrop has sparked a discussion about the divergence between private and public markets. The large-scale private placement and high FDV airdrop model based on points are bringing structural problems to the cryptocurrency industry.

Transforming point systems into tokens worth billions of dollars with low circulation is not in a stable balance, yet we are still trapped in this model due to the convergence of various factors: excess venture capital, lack of new participants, and excessive regulation.

Meta about token issuance is always changing, and we have witnessed several major eras:

2013: Proof of Work (PoW) fork and fair release meta

2017: Initial Coin Offering (ICO) meta

2020: Era of liquidity mining (DeFi summer)

2021: NFT minting

2024: Points and airdrop metaverse

Each new token distribution mechanism has its advantages and disadvantages. Unfortunately, this particular meta starts from a structural retail disadvantage, which is an inevitable consequence of the industry being ruthlessly regulated.

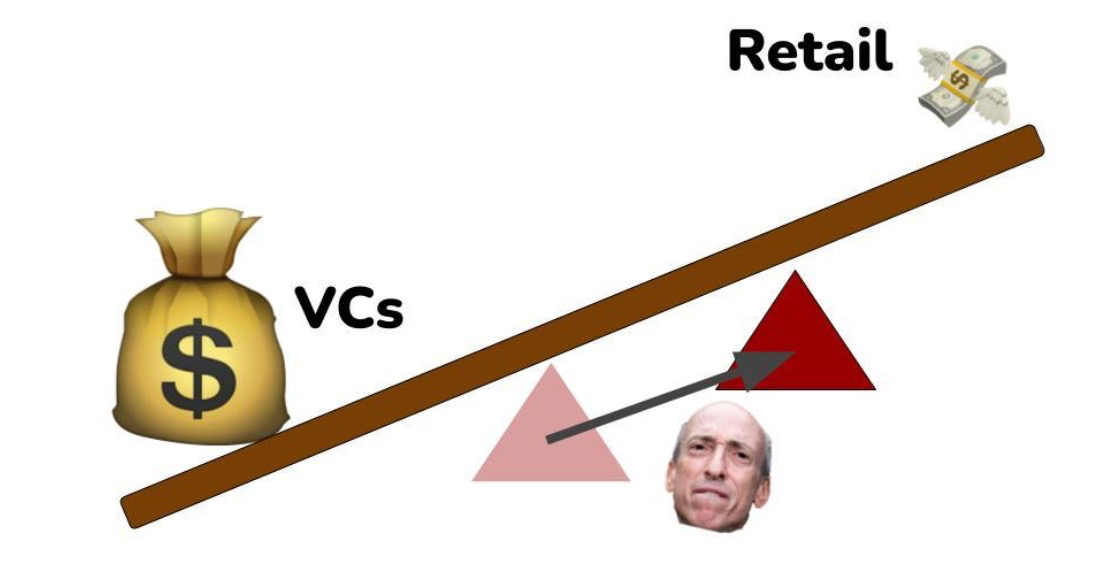

A large amount of venture capital and retail investors

Currently, there is an oversupply of venture capital in the cryptocurrency industry. Although 2023 was a bad year for venture capital fundraising, the financing in 2021 still saw a large amount of funds, and overall, financing in the cryptocurrency field is a persistent and continuous activity.

At present, many well-funded venture capital firms are still willing to continue leading with valuations of billions of dollars, which means that cryptocurrency startups have an increasingly long time to remain private. Of course, this is reasonable, because if the current token issuance price is a multiple of the last financing, even later venture capitalists can still find a good deal.

The problem is that when a startup issues tokens publicly at a valuation of 10 billion to 100 billion dollars, most of the upside potential has already been discovered by early participants—meaning, no one will get rich by buying a token worth 100 billion dollars.

The structural bias against public market capital is detrimental to the overall atmosphere of the cryptocurrency industry. People want to get rich with their internet friends and form strong online communities and friendships around this activity. This is the promise of crypto, a promise that has not been fulfilled.

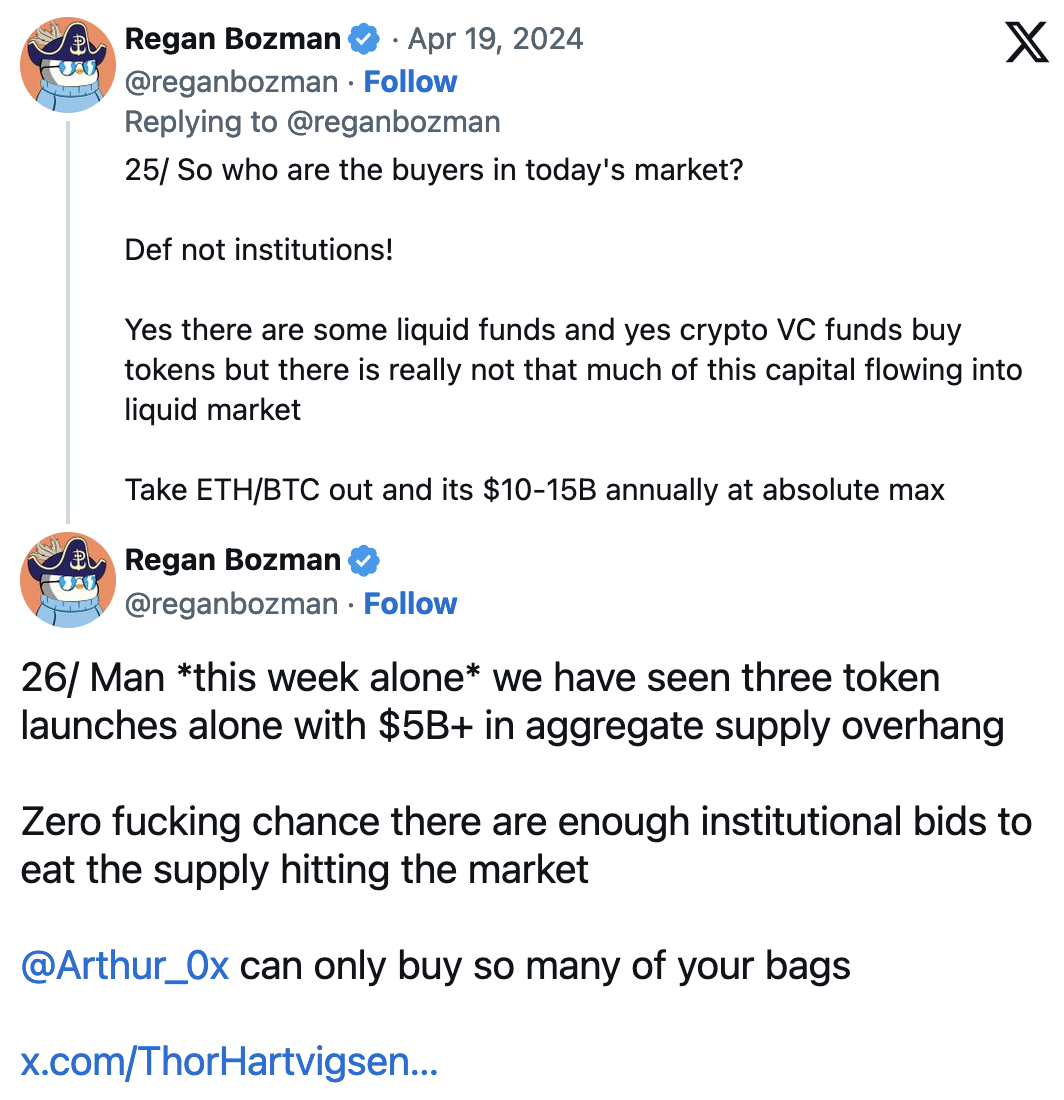

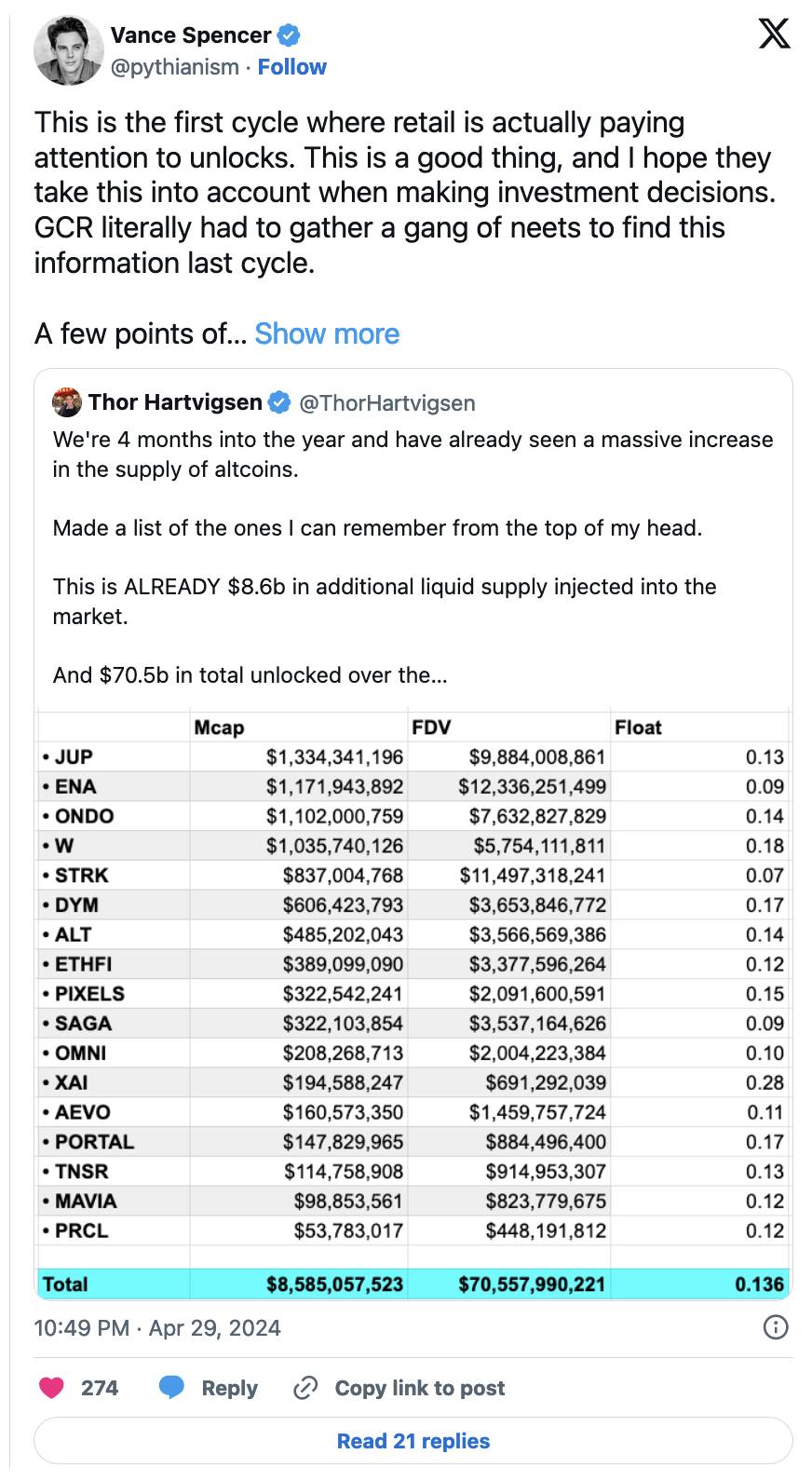

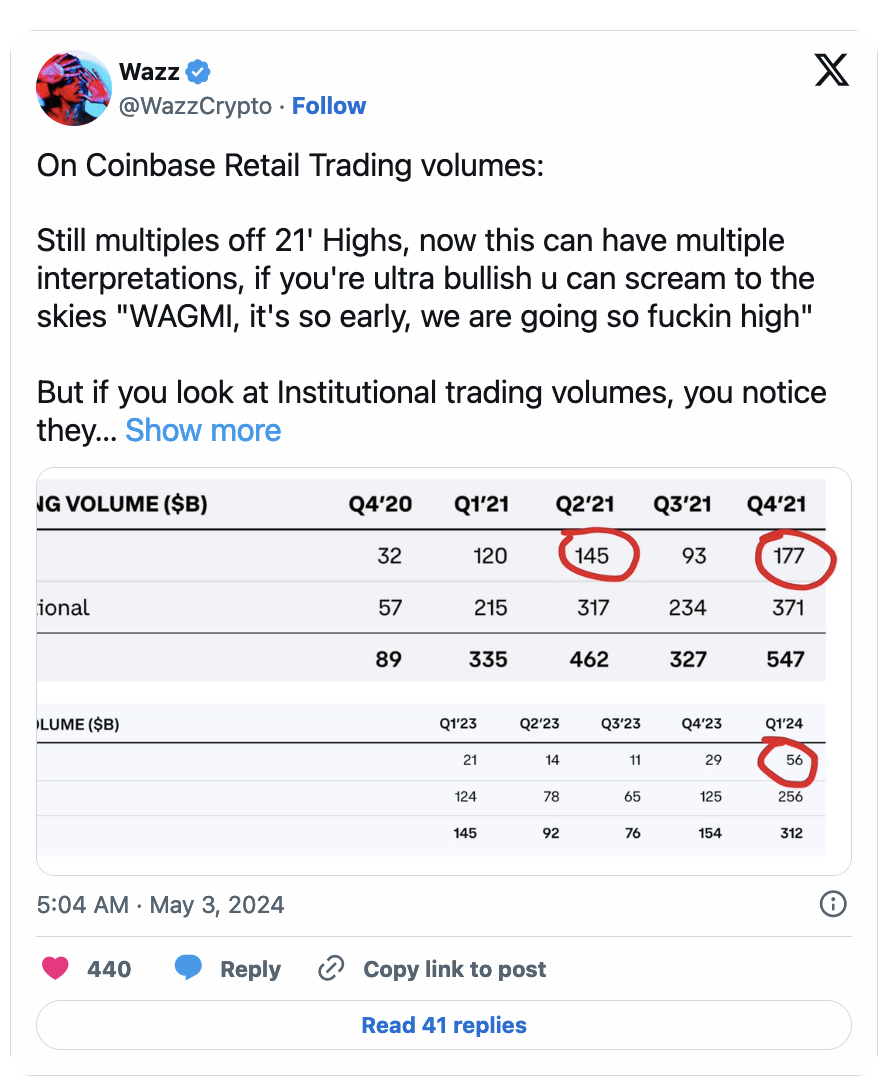

Facing billions of unlocks without new participants

Several data points should make you start thinking:

Due to the long tail of retail investors holding most of the crypto assets, institutional liquidity entering through a Bitcoin ETF will not impact these markets. Capital recirculation from native crypto players selling their BTC bought at $14,000 to Larry Fink can temporarily support these assets, but this is internal capital from players with PVP capabilities who understand the unlocking mechanism and how to avoid it.

Impact of the U.S. Securities and Exchange Commission (SEC)

By restricting the ability of startups to raise capital and distribute tokens more freely, the SEC is encouraging capital to flow to less regulated private markets.

The SEC's corrupt and excessive attitude towards the nature of tokens is undermining the value of public market capital, as startups cannot exchange tokens for public market capital without triggering massive bleeding from legal teams.

Compliance Process in Crypto

Over time, crypto has gradually become more compliant. When I entered the crypto space during the ICO frenzy in 2017, ICOs were touted as a democratized way of investing and raising capital. Of course, ICOs eventually evolved into a scam, but regardless, this story forced me and many others to realize the potential that cryptocurrencies could bring to the world. However, when regulatory agencies viewed these transactions as clear cases of unregistered securities sales, the ICO meta came to an end.

The industry then shifted towards liquidity mining, going through a similar process.

Each cycle, cryptocurrencies manage to obscure their methods of distributing tokens to the public, and each cycle, hiding this process becomes more difficult—this process is crucial for the decentralization of projects and the nature of our industry.

This cycle has faced the most ruthless regulatory scrutiny we have ever seen, so lawyers for venture-backed startups are facing the industry's biggest compliance challenge ever: distributing tokens to the public without being sued by regulatory agencies.

Breaking the Balance

Regulatory compliance severely tilts the pivot between public and private markets towards the private market, as startups can choose to accept venture capital directly rather than violate securities laws.

The position of the pivot supporting the balance of private and public capital is determined by the regulatory control of the cryptocurrency market.

If there were no accredited investor laws, this pivot would be more balanced.

If there were clear regulatory pathways to issue tokens compliantly, the difference between public and private markets would be smaller.

If the SEC did not participate in the war on cryptocurrencies, we would have a fairer and more orderly market.

Due to the lack of clear rules from the SEC, we have ended up with a complex and confusing "point" meta that satisfies no one.

Unfair Points, Market Disorder

"Points" leave retail investors unaware of what they are actually receiving, because if there were a clear statement of what points actually are (debt to tokens), the team would expose themselves to potential violations of securities laws (from the perspective of a corrupt and overreaching SEC regulator).

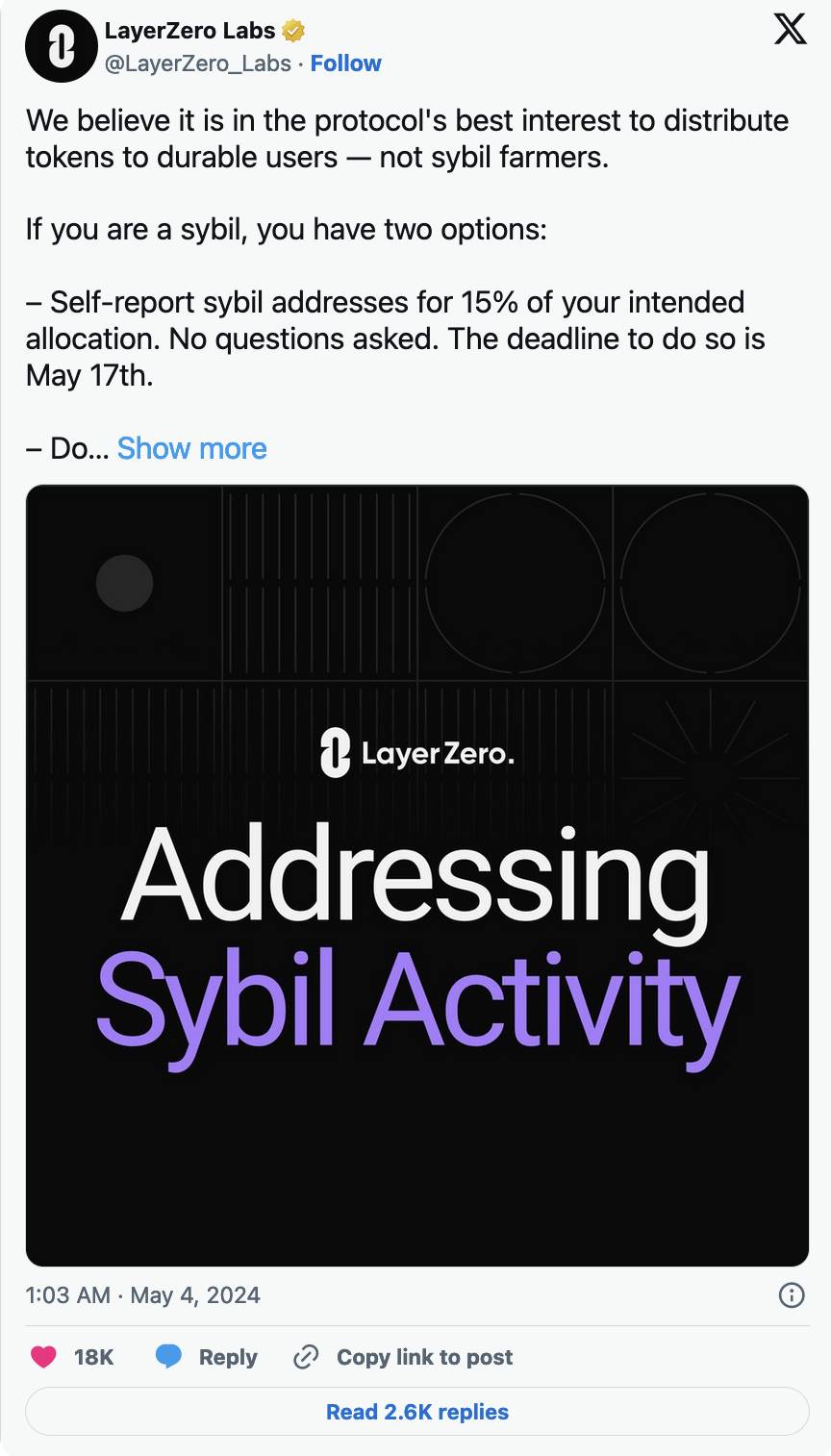

Points do not provide investor protection, as providing investor protection first requires giving this process regulatory legitimacy. Finding ourselves in this extremely dire conclusion, we have found ourselves in a debate between witches and the community, where LayerZero is caught in a dilemma.

LayerZero recently announced a plan that allows users to report witch behavior in the LayerZero airdrop through self-reporting, prompting Kain Warwick to write this post defending the witches, as the witches have to some extent supported LayerZero and elevated its position in the market.

In reality, there is no boundary between community members and witches. Since regular crypto participants cannot participate in private sales, the only way they can gain exposure is by engaging in commitments and meaningful activities on platforms where they want tokens.

As there is no simple way for small investors to write small checks to crypto projects in the early stages, the current token issuance mechanism forces users to engage in witch behavior for projects they believe in. Therefore, in this cycle, no "community" will come together to get rich as with LINK in 2020 or SOL in 2023. The current token issuance does not allow the community to gain early exposure at undervalued prices.

As a result, attacks on airdropped startups on Twitter are becoming more common—this is the inevitable result of the community's inability to express its desires as effective stakeholders in projects. It has the meaning of "no representation, no taxation!"

Not to mention another potential issue: profit-seeking capital exploitatively gaining tokens and dumping them. In the absence of the ability for small investors to invest in early stages of startups, these highly coordinated investors must compete with toxic rent-seekers in airdrops, with no discernible difference between the two.

Inappropriate Balance

The "point" meta has become too obvious to sustain. Both the SEC and scammers are working towards this, and both are trying to use it for their own gain.

We will have to turn to a different strategy, hoping that this strategy will make many early community stakeholders wealthy without angering the SEC. Unfortunately, this is a pipe dream without regulatory provisions for token issuance.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。