1. 研究介绍

1.1 研究背景

今年以来,市场对高完全稀释估值(FDV)但低流通市值(MC)的VC代币引发了广泛讨论。随着2024年新发行的代币,MC/FDV比率降至过去三年的最低水平,这表明未来将有大量代币解锁进入市场。尽管初期流通量较低,市场在短期内可能会因为需求增加而推动价格上涨,但这种上涨缺乏持续性。一旦大量代币解锁并进入市场,供应过剩的风险加剧,投资者开始担忧这种市场结构可能无法为价格上涨提供持久的支持。

因此,许多投资者的兴趣开始从这些VC代币转向Meme币。Meme币的特点是大部分代币在TGE时就已完全解锁,流通率较高,没有未来解锁带来的抛售压力。这种结构减少了市场的供应压力,给予投资者更多的信心。许多Meme币在发行时的MC/FDV比率接近1,意味着持有者不会因代币进一步发行而面临稀释,提供了一个相对稳定的市场环境。随着对大规模代币解锁风险的认识加深,投资者的兴趣逐渐转向了这些流通性较高、通货膨胀率较低的Meme币,尽管这些代币可能缺乏实际的应用场景。

当前的市场格局中,要求投资者必须更加谨慎地选择代币。然而,投资者在挑选代币时,往往难以独立评估每个项目的价值和潜力,这时,交易所的筛选机制成为了关键。作为直接将代币资产推向用户的“守门员”,中心化交易所不仅帮助验证代币的合规性和市场潜力,还起到了筛选优质项目的作用。尽管市场中拥有另外一种声音,即链上的交易将会超过CEX的交易。但Klein Labs认为,中心化交易所的市场份额占比不会被链上交易夺取。CEX的交易丝滑程度、中心化的有责资产托管、用户习惯与心智的建立、流动性的壁垒、全球监管的合规趋势等因素,使得CEX中的交易份额将长期而持续地超过链上的交易份额。

那么,随之而来的问题是,中心化交易所如何在众多项目中筛选并决定上线?在过去的一年中已经上线的币种整体表现怎么样?这些上线的代币表现和选择的交易所已是否有关?

为了回答市场关心的这些问题,本研究旨在探讨各大交易所的上币情况,并分析其对代币市场表现的实际影响,重点关注上币后的交易量变化及价格波动特征,以识别不同交易所对币种上线后市场表现的影响。

1.2 研究方法

1.2.1研究对象

我们将交易所结合地域与面向市场,主要分为这三类:

华人创建,面向全球:Binance、Bybit、OKX、Bitget、KuCoin、Gate等。主要由华人创办投资的知名交易所,面向全球市场。华人交易所数量较多,为便于研究,选取的交易所有不同的发展特色,未被选取的交易所同样也有各自的优势。

韩国创建,面向本土:Bithumb、UPbit等。主要面向韩国本土市场。

美国创建,面向欧美:Coinbase、Kraken等。美国交易所,主要面向欧美市场,通常受SEC、CFTC等严格监管。

拉美、印度、非洲等其他地区交易所,由于交易量、流动性整体小于5%,因而在本研报中不进行深入分析。

我们选取了以上共10家交易所具有代表性的交易所,分析其上币表现,包括上币事件数量及其后续市场影响。

1.2.2 时间范围

主要关注代币TGE之后第1天、前7天及前30天的价格变化,分析其趋势、波动模式及市场反应,原因如下:

- 在TGE的首日,新资产发行,交易量高度活跃,反映市场的即时接受度。受抢筹和FOMO情绪影响较大,是市场初始定价的关键阶段。

- TGE之后前7天的价格变化可以捕捉市场对新代币的短期情绪,以及对项目基本面的初步认可,衡量市场热度的持续性,并回归到项目的合理初始定价。

- TGE之后前30天则观察代币的长期支撑力,短期炒作降温,投机者逐渐退出,代币价格与交易量是否维持,成为市场认可度的重要参考。

1.2.3 数据处理

本研究采用系统性的数据处理方法,以确保分析的科学性。相对于市面上常见的研究方法,本研究更具有直观性,简洁性和高效性。

本研报中,数据主要来自 TradingView,涵盖2024年各大交易所新上线代币的价格数据,包括上币初始价格、不同时间点的市场价格及交易量等数据。由于样本点较多,这种大规模数据分析有助于降低单一异常数据对整体趋势的影响,从而提高统计结果的可靠性。

( I )多变量概述上币活动

本研究采用多变量分析方法,综合考虑市场行情、交易深度、流动性等因素,以确保结果的全面性和科学性。我们对比了不同交易所新币的平均涨跌幅,并结合交易所的市场定位(如用户基数、流动性、上币策略)进行深入分析。

( II )平均值判断整体表现

为衡量代币的市场表现,我们计算了其相对于上币初始价格的百分比变化(Percentage Change),计算公式如下:

考虑到市场中的极端情况可能会影响整体数据趋势,我们剔除了前 10% 和后 10% 的极端异常值,以减少偶发性市场事件(如突发利好、市场操纵、流动性异常)对统计结果的干扰。这种处理方式使得计算结果更加具代表性,能够更准确地反映新币在不同交易所的真实市场表现。随后,我们计算各交易所新币涨跌幅的均值,以衡量不同平台新币市场的整体表现。

(III)变异系数判断稳定性

变异系数(Coefficient of Variation, CV)是衡量数据相对波动性的指标,其计算公式为:

其中,σ为标准差,μ为均值。变异系数是无量纲指标,不受数据单位影响,适用于不同数据集的波动性比较。在市场分析中,CV 主要用于衡量价格或收益的相对波动性。在交易所或代币价格分析中,CV 能够反映不同市场的相对稳定性,为投资者提供风险评估依据。此处使用变异系数而非标准差。因为变异系数相较于标准差具有更高的适用性。

2. 上币活动概述

2.1 交易所间对比

2.1.1 上币数量与FDV偏好

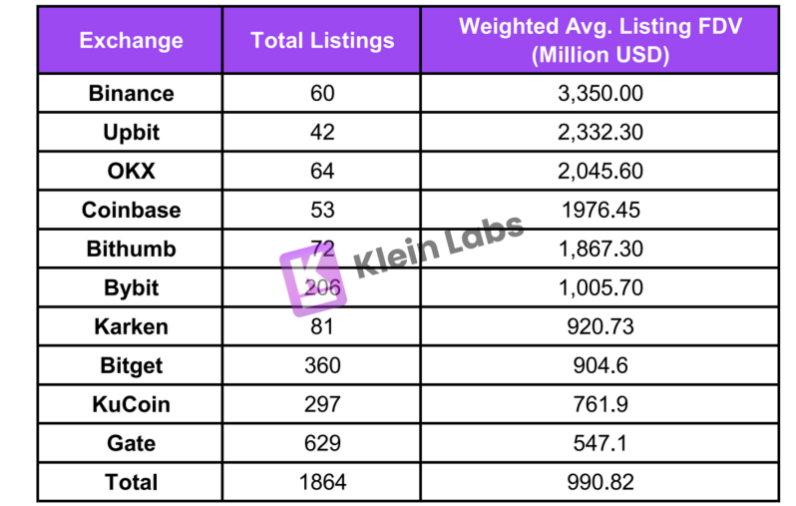

2024年上币事件概述我们发现:从整体数据上来看顶级交易所(如Binance、UPbit、Coinbase)上币数量普遍少于其他交易所。这体现交易所所处地位的不同影响上币风格。

从上币数量来看,如 Binance、OKX、UPbit、Coinbase,上币规则更为严格,上币数量较少但规模较大;而 Gate等交易所则更频繁地上币新资产,提供更多交易机会。数据显示,上币数量与 FDV大致呈负相关,即上更多高 FDV 项目的交易所通常上币数量较少。

CEX所采用不同的策略来确定上币优先级,重点关注不同的完全稀释估值(FDV)层级。这里我们根据项目的FDV不同进行分类,以便于更好理解交易所上币的标准。代币估值时,我们常常考虑 MC和 FDV,它们共同反映代币的估值、市场规模和流动性。

- MC 仅计算当前流通代币的总价值,未考虑未来解锁的代币,因此可能低估项目的真实估值,尤其是在大部分代币尚未解锁时,容易造成误导。

- FDV 则基于所有代币总量计算,能更全面反映项目的潜在估值,有助于投资者评估未来的抛压风险及长期价值。对于低MC/FDV的项目来说,FDV的短期参考意义有限,更多是长期参考。

因此,在分析新上线代币时,FDV 比 Market Cap 更具参考性。这里我们选择FDV作为标准。

此外,从对于首发项目的态度来看,通常大多数交易所采用了均衡策略,即兼顾首发、非首发项目,但是通常对非首发项目的要求更高,因为首发项目会带来的新用户更多。此外,两家韩国交易所 UPbit 和 Bithumb 主要专注于非首发上币。因为相比首发,非首发上币可以降低筛选风险,还能规避首发阶段的市场波动和初期流动性不足的问题。同时,对于项目方,相比首发,项目方不需要承担过多市场推广和流动性管理压力,非首发上币能借助已有市场认可度推动增长。

2.1.2 赛道偏好

- Binance

2024年,Meme币数量仍然占比最多。Infra与DeFi项目占比较大。RWA 和 DePIN 赛道在 Binance 上币数量相对较少,但整体表现较好。其中USUAL 现货最高涨幅达 7081%。尽管 Binance 在这些领域的上币选择较为谨慎,但一旦上线,市场反应通常较为积极。在下半年,Binance在AI赛道的上币偏好明显向AI Agent代币倾斜,其占比在AI类项目中最高。

2024年,Binance 比较偏好 BNB 生态。例如,BANANA 和 CGPT 等项目的上线,表明 Binance 在加强对自身链上生态的支持。

- OKX

OKX上币数量上看同样Meme数量最多,占比约25%。而相比其他交易所,在公链和基础设施赛道上币更多,合计占比高达34%,这说明相比之下,OKX在2024年更关注底层技术创新、扩展性优化和区块链生态可持续发展。

在新兴赛道上,OKX只上线了4种AI代币,包括DMAIL与GPT,在RWA赛道上线了3种新代币,在DePIN赛道只有3种。这反应OKX在相对新兴赛道的布局较为谨慎。

- UPbit

UPbit 2024年上币最大特点是赛道覆盖广泛,代币表现普遍较好。在2024年,在DEX赛道上线了UNI和BNT。这说明 UPbit 在热门资产的上架上仍有较大潜力和发展空间,许多主流或高市值代币尚未上线,未来可能进一步扩展支持。同时,这也反映出 UPbit 对上币审核较为严格,更倾向于慎重筛选具备长期潜力的资产。

在UPbit上,各赛道的代币涨幅都比较突出。PEPE(Meme)、AGLD(Game)、DRIFT (DeFi )、SAFE (Infra)等赛道的代币在短期内涨幅显著,最高达 100% 甚至超过 150%。UNI在上线第30天后和第1天相比涨幅高达93.5%。这反应出韩国用户对UPbit上线项目有极高的认可度。

此外,从公链生态的角度,Solana、TON等公链生态较为受宠。我们还观察到,交易所正逐步加深对自身区块链生态的支持。例如Binance 关联的 BSC 和 opBNB 链,其对自身链上生态的扶持力度持续增强。同样,Coinbase 推出的 Base 也成为其重点支持对象,在2024所有新上线币种中Base项目占比接近40%。而 OKX 则在 X Layer 生态布局上持续发力。此外,Kraken 计划推出的 L2 网络 Ink 进一步表明,头部交易所正积极推进链上基础设施建设。

这种趋势的背后,是交易所从“链下”向“链上”转型的探索,不仅拓展了业务范围,也强化了其在 DeFi 领域的竞争力。交易所通过支持自身链上的项目,不仅能推动生态发展,还能提升用户粘性,并在新资产的发行和交易过程中获取更高的收益。这也意味着,在未来,交易所的上币策略将更加偏向于自身生态体系内的项目,以增强其区块链网络的活跃度和市场影响力。

2.2 时间维度分析

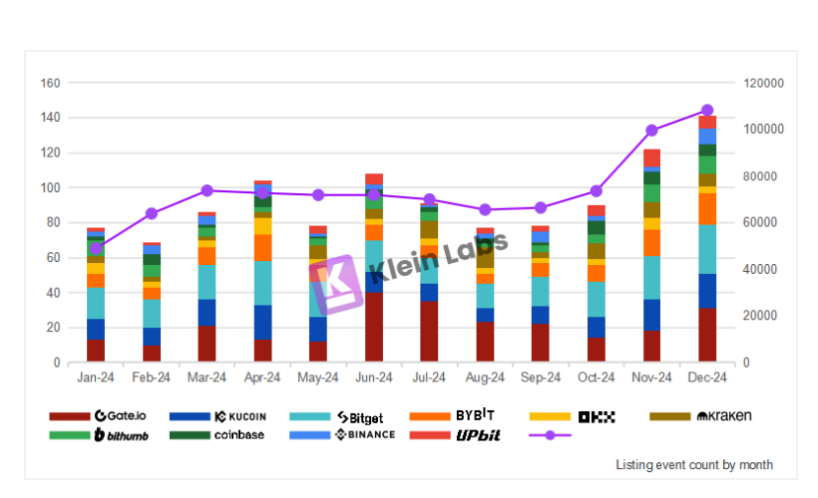

不同交易所每月的上币数量情况- 上币事件数量的增减趋势与BTC价格涨跌高度一致。BTC上涨期间(2月至3月和8月至12月)上币事件较多,而BTC横盘或者下跌期间(4月至7月)上币事件数量明显减少。

- 顶级交易所(Binance、UPbit)的上币活动在熊市期间受影响较小,其上币份额在此期间反而有所扩大,显示出更强的市场主导力和抗周期能力。

- Bitget 上币数量较稳定,市场波动对其影响较小,而其他交易所的上币节奏波动较大。可能与其更均衡的上币策略相关。

- Gate和KuCoin具有更高的上币频率,但上币数量随市场行情波动较大,表明这些交易所可能更依赖牛市时新项目较高的流动性来吸引用户。

3. 交易量分析

3.1 不同交易所交易量总体情况

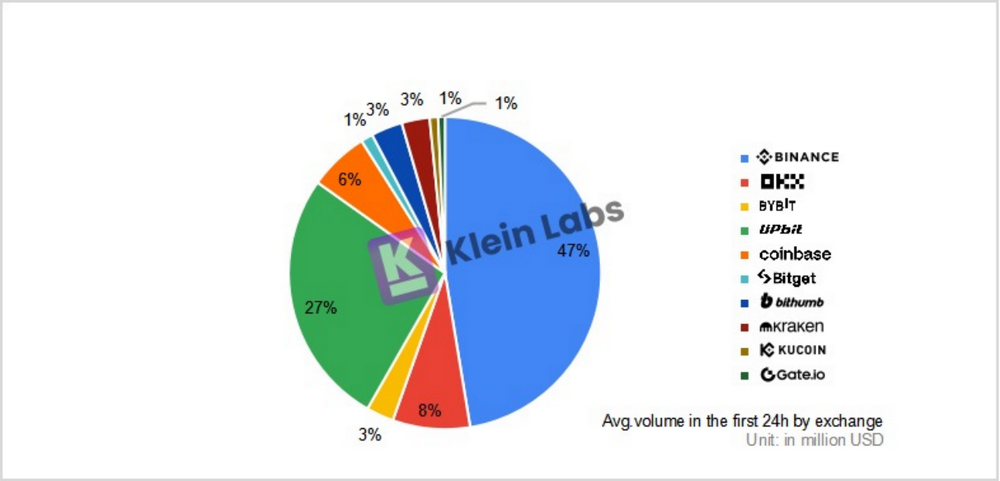

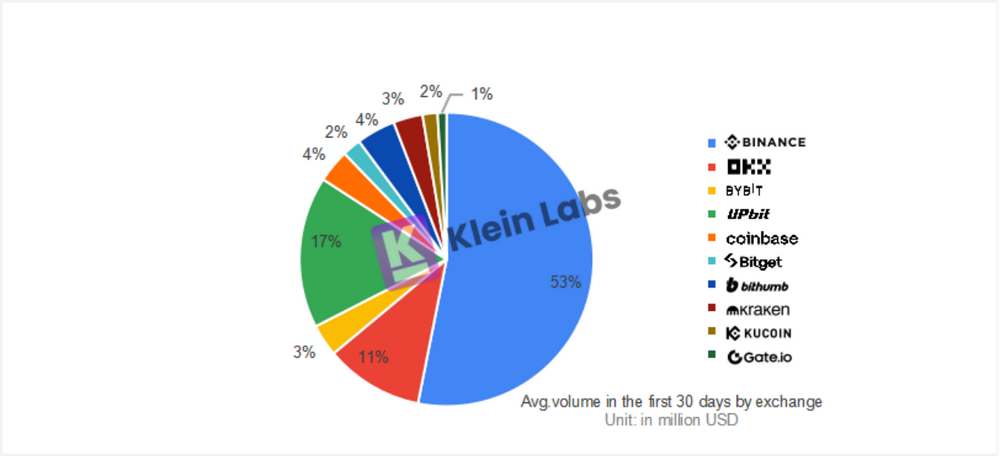

2024年各交易所项目TGE后24小时的平均交易量

2024年各交易所项目TGE后30天的平均交易量- UPbit 在币种上市 24 小时内交易量占比极高,甚至超过 Binance 的一半,显示出其在短期市场的强大吸引力,流动性涌入明显。虽然 30 天后占比略有下降,但仍保持较高市场份额,占比甚至接近 OKX、Coinbase、Bybit三个顶级交易所的份额总和,表明 UPbit 在上币市场中占据极为重要的地位。

- Binance 和 OKX 交易量稳健增长,30 天市场份额仍然领先,显示出强大的市场认可度和流动性深度。Binance 在 24 小时内占比 47%,30 天后更是增长至 53%,表明其长期市场主导地位,而 OKX 也在 30 天后维持较高份额。

- Bybit 在短期和长期交易量均表现良好,较为稳定。而Bithumb 市场份额在 30 天后略有上升,表明其不仅能够留住早期交易量,还能吸引更多流动性。这说明 Bithumb 在上币市场中的竞争力有所增强。

尽管韩国交易所以偏好非首发项目而闻名,但正如以上数据显示,这些项目依然能够带来十分强劲的交易量。韩国交易所的非首发项目能够产生如此庞大的交易量,核心原因在于其独特的市场环境:

韩国交易市场的封闭性与流动性集中

- 市场封闭:由于韩国本土KYC政策较为严格,海外用户基本无法直接使用韩国的交易所,这种区域隔离导致韩国市场形成相对封闭的交易生态;大量本土用户习惯在韩国交易所进行买卖。因此韩国市场内部流动性更集中。

- 交易所垄断:韩国加密市场呈现高度垄断格局,UPbit目前占据 70%-80% 的韩国加密市场份额,稳居行业龙头。2021 年 UPbit 确立领先地位后,Bithumb原来第一的地位被取代,市场份额下降至 15%-20%。韩国交易量与流动性向头部平台聚拢,展现出强大的资金聚集效应。

因此,尽管一个代币在全球市场上已非首次上市,但在韩国市场上的交易情况仍会呈现出类似“首发”的效应,带动大量的市场关注和资金流入。

韩国加密市场的高持有率与资本优势

- 加密资产的高渗透率:韩国投资者对加密货币的持有比例极高,远高于其他主要市场,截止到2024年11月统计,在韩国交易所持有加密货币的人数超过1559万人,相当于韩国总人口的30%以上。许多韩国人本身就持有大量加密资产,并且在投资选择上更倾向于数字资产。韩国以全球0.6%的人口,贡献了全球30%的加密货币交易量。

- 社会资本充足:再加上韩国是GDP较高的发达国家,整体社会资本较为充裕,可投资资金庞大,使得加密市场具备充足的流动性。

- 传统行业年轻人的生存空间较小:韩国为财阀垄断的资本主义国家,年轻人面临较大的就业和生活压力,阶层固化加剧了对财富增值渠道的渴求。约有308万名20-39岁的年轻人参与虚拟货币交易,占该年龄段总人口的23%。

截止到2024年11月,韩国民众对加密货币的总持有量已增至102.6万亿韩元(约合697.68亿美元),日均交易额也攀升至14.9万亿韩元(约合101.32亿美元)。UPbit在2024年第四季度成为交易量增长最快的CEX,从1355亿美元增加至5619亿美元,环比增长了314.8%。这一增长反映了韩国市场对加密资产的强劲需求,也进一步佐证了韩国交易所在非首发项目上的高交易量趋势。

4. 价格表现分析

4.1 按交易所对比的价格表现

4.1.1 各交易所上币价格总体表现

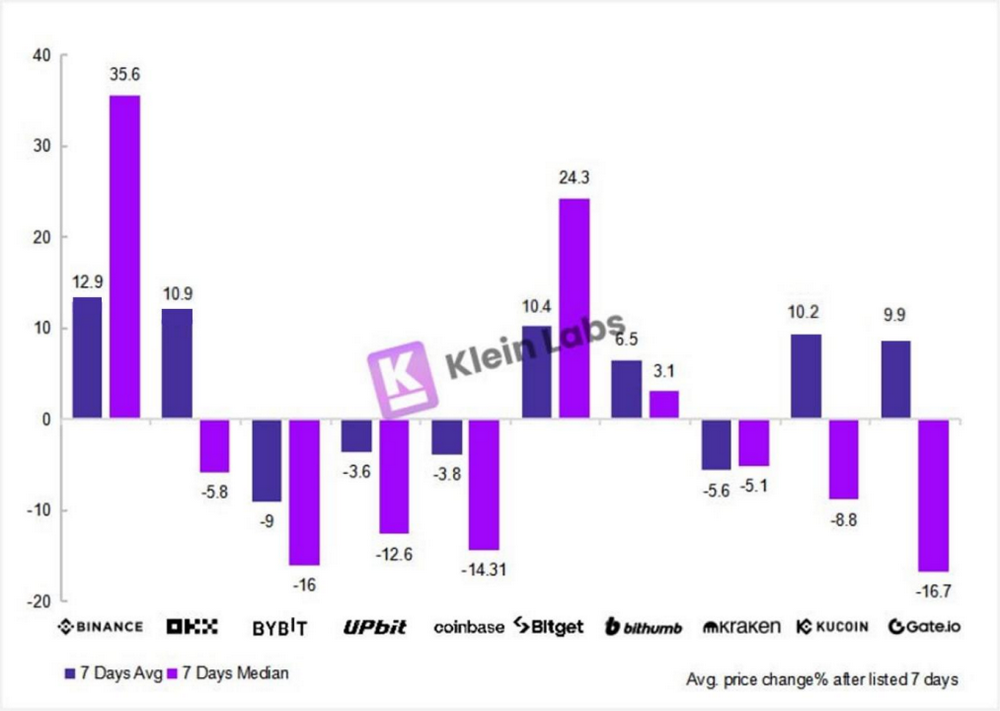

各个交易所TGE后7天的交易量价格均值与中位数比较- Binance表现最好,平均值和中位数都比较突出。平均值排名前三依次是Binance,OKX,Bitget,其中OKX虽然平均值正,但中位数为负,表明上涨代币的价格波动大,在短期内的价格波动很剧烈,异常值较明显。Bitget表现较为突出,在其他交易所中最接近两大头部交易所。同时,其中位数涨幅位列所有交易所第二,仅次于 Binance,且呈现较高的正数值,这表明 Bitget 上的代币价格整体呈现有力的、正向的上涨趋势。

- 中型交易所中,Bithumb,Gate,KuCoin三者表现较好。其中,Bithumb是价格表现较为均衡的一个,绝对值和中位数差值最小,说明价格波动较小,表现稳定。但是其中KuCoin,Gate的中位数为负数,并且绝对值较高,这说明代币胜率较低,且可能出现了较多上涨异常值进行干扰。

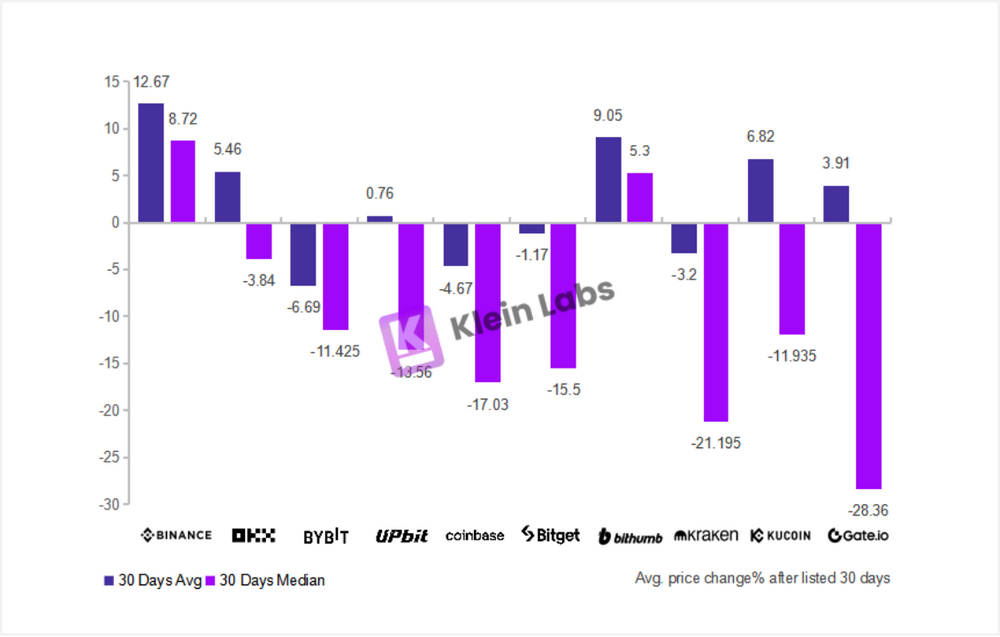

各个交易所TGE后30天的交易量价格均值与中位数比较- 到第30天,整体上中位数都下跌,这说明30天后,尤其是对于流动性较差的代币来说,市场上部分投机资金撤出较多,卖盘的压力加大,买盘支撑不足,价格下跌。Gate可能由于上币数量过多,导致新币市场波动较大,流动性不足。这表明平台未能吸引足够的稳定资金流入,过多的代币选择分散了流动性,买卖双方的平衡被打破,造成价格大幅下跌。

- Binance受到影响较小,平均值略微下降,说明其上线代币在30天后,仍然保持较强的市场支持和稳定的交易量,部分代币仍然有上涨空间。Binance作为顶级交易所,凭借其庞大的市场流动性和广泛的用户基础,即便30天后新币市场整体下行,其平台上的代币价格依然能维持较高水平。

- 中型交易所中,Bithumb 是唯一在30天后上涨的交易所,并且7天涨幅和中位数均为正。这表明Bithumb凭借较好的市场流动性和稳定性,成功吸引资金,表现出较强的抗跌性和市场吸引力。可能是因为Bithumb较少的上币量让它能够集中流动性,保持较强的市场活跃度,使得新上市代币能够在价格上表现更好。

4.1.2 各交易所每月上币价格表现

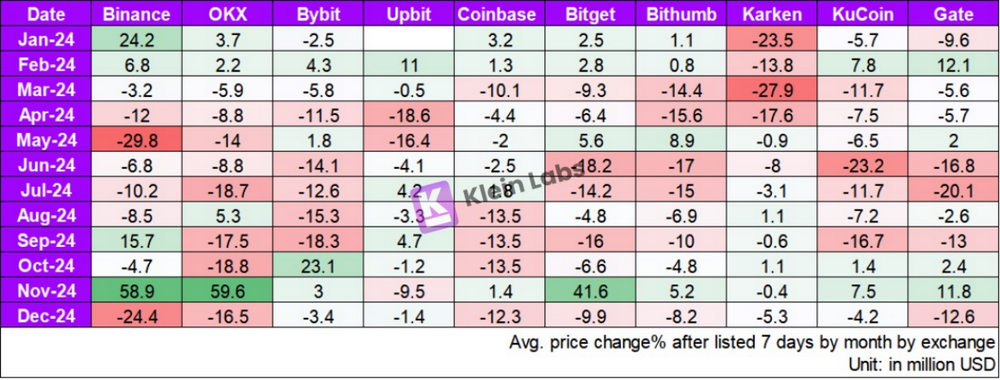

各个交易所TGE 7天后,每个月每个交易所的价格变化情况- Binance 和 UPbit 价格优势明显,受市场情绪影响大。Binance 和 UPbit 的上币在市场行情向好时表现突出,例如 5 月和 9 月 Binance 30 天涨幅分别达到 87.8% 和 94.9%,UPbit 9 月也有 60.5% 的涨幅,显示出较强的价格优势,但波动性较大,在 4 月和 7 月出现明显跌幅,市场情绪对其影响显著。

- 市场整体行情对代币走势影响明显,顶级交易所的上币在牛市时涨幅更大,而中型交易所则更易在市场低迷时出现大跌。例如 Bybit 和 OKX 在 7 月 30 天跌幅分别达到 -40.6% 和 -36.6%,Kraken 和 KuCoin在7 天后的整体表现也较弱,特别是 Kraken 在 1 月和 3 月跌幅分别达到 -23.5% 和 -27.9%。

4.2 涨跌幅波动情况

我们在上一部分用平均值反映了整体的涨跌幅高低。那么接下来用变异系数来反应样本数据围绕上面平均涨跌幅的波动情况。若变异系数较小,说明数据分布较为集中,大多数代币的涨跌幅接近平均水平,市场表现较为稳定,交易所上币后的价格波动可预测性较强;反之,则交易所上币后的价格走势更具不确定性;

接下来将1天,30天的价格分别分析:

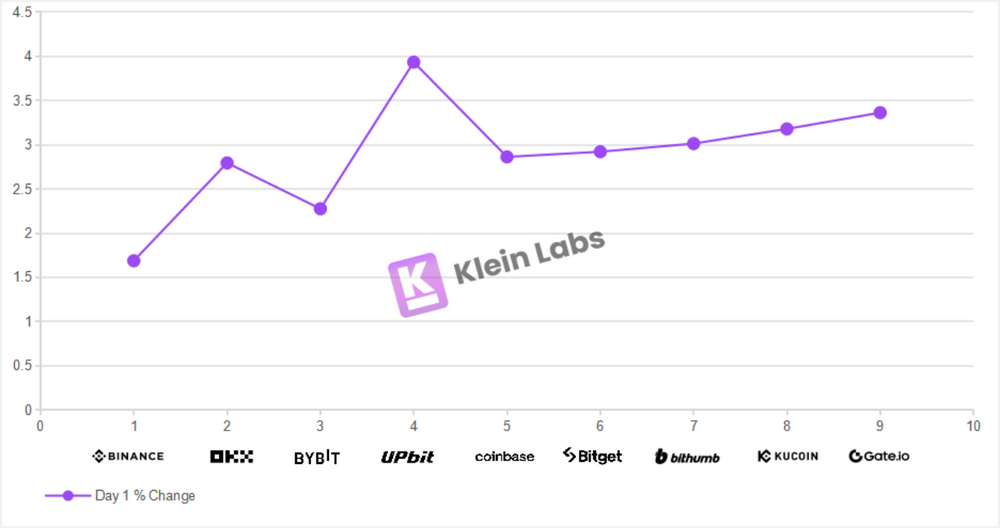

变异系数在TGE后第1天的变化情况- Binance 变异系数最低,表明其上线代币的首日涨跌幅波动相对较小,市场表现最稳定。UPbit 变异系数最高,首日波动较大,但结合此前的平均值分析,估计其市场总体大概率呈现普遍上涨趋势。

- 中型交易所(沿坐标轴从左向右)变异系数呈现线性增长趋势。从变异系数最低的Bitget,到变异系数最高的Gate。表明这些交易所的上币市场表现从较为稳定逐步趋向于更高的不确定性,从短期投资风险相对较低到逐渐提升。

- Bybit 变异系数较低,与 Binance 最接近,表明其市场波动性也相对可控。然而,考虑到 Bybit 的上币数量较多,仍能保持较低的变异系数,说明其上线项目的整体质量较高,未出现大规模的高波动币种。此外,这也反映出 Bybit 在上币筛选策略上可能更倾向于稳定性较强的代币,从而降低市场短期内的剧烈波动。

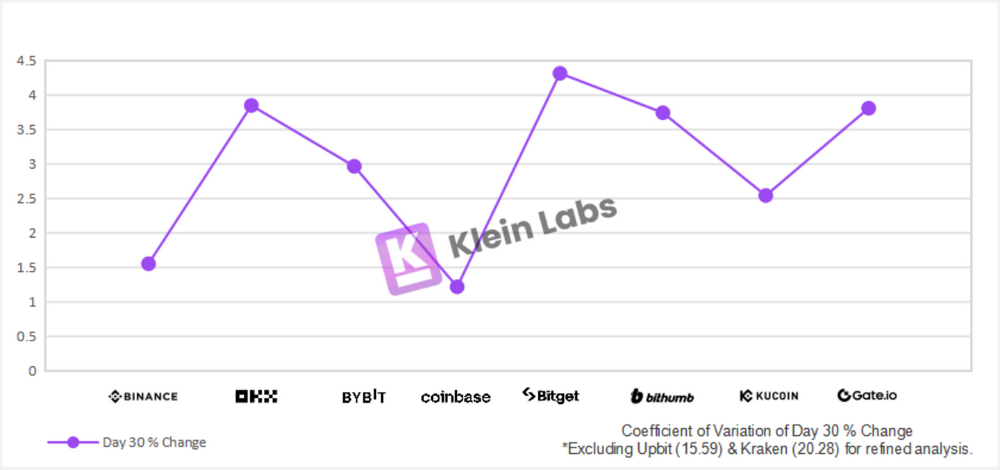

变异系数在TGE后第30天的变化情况- 从 Day 30 变异系数来看,UPbit 在 7 天和 30 天后仍保持较高的变异系数,说明其交易对价格波动显著,市场流动性较高。结合平均值观察,UPbit 交易对的平均值为正,且价格下降较为缓慢,这表明市场买卖盘较为活跃,流动性深度足够强大,整体市场健康。从变异系数的角度来看,UPbit 在这一点上相较于其他交易所有较大的优势。

- Binance 和 Coinbase 仍然是较为稳定的交易所,Binance 在整个周期内涨幅较为稳定,而 Coinbase 在 7 天到 30 天之间波动趋于稳定,表明其代币市场更倾向于长周期稳健发展,而非短期剧烈波动。

- 中型交易所(如 Bitget、Bithumb、Gate、KuCoin)在第 30 天的变异系数大幅上升,说明短期套利资金撤离后,流动性下降,导致价格波动加剧。市场仍以短线资金为主,长期资金占比较低,整体稳定性较弱。尤其是 Bitget,活跃度高但波动风险较大。

5. 亮点总结

5.1 数据结论

经过以上研究和数据,我们得出以下结论:

1. 交易所上币选择对上币表现影响显著

普遍来看,上币较少,较为严格的交易所,在去除极端异常值之后价格表现通常会更好。然而,整体比特币走势、地区市场环境和用户特征也会影响上币表现。

上币数量较多的交易所,确实在短期平均值表现中会相对突出,但从长期来看,上币较多造成流动性更加分散,在30天后可能会迎来更大的回落,价格稳定性较低。

2. 顶级交易所在市场行情好时,往往和中型交易所相比有更大的涨幅优势

但是从另一个指标,从涨幅平均值看来,各大顶级交易所在7天,30天上的涨幅表现各异,但是总体为正。Binance在各项价格指标中反馈最好。OKX中长期来看波动较大。顶级交易所中,UPbit的表现最为平缓,这可能由于流动性深度较大。同时UPbit实际上在代币上线首日内可达到极高的涨跌幅。但是由于本研究统计第一天最终收盘价,可能未记录这些突出表现。中型交易所中Bitget和Bithumb表现较为突出。其中Bitget表现稳定,Bithumb在部分价格指标表现突出。

3. 韩国市场的优势和上币效应

韩国市场拥有独特的市场环境,交易量高,流动性好,代币上币后能快速吸引资金。尽管初期价格波动较大,但总体呈上涨趋势。并且在7天,30天后价格波动仍然剧烈。说明在韩国市场上,代币上线会获得更长的发展周期和更高的关注度。

4. 交易所筛选流程对代币表现和市场稳定性的影响

在数据处理过程中,我们发现某些交易所的异常值明显较多,表明代币筛选和审查流程对上市后的表现至关重要。异常值通常反映代币价格偏离预期,可能受到市场操控或项目风险等因素的影响。频繁出现异常值的交易所可能在筛选过程中较为宽松,导致不稳定代币进入市场,增加价格波动风险。因此,交易所的代币筛选流程直接影响代币的市场表现和整体市场稳定性。

5.2 交易所表现

Binance & OKX

在各项指标上都表现出色,但从长期来看,Binance在稳定性方面更具优势。Binance的市场表现较为稳定,能够保持持续的增长,并且波动性较小。相比之下,OKX虽然在市场波动性上较Binance更大,但其在多个指标上几乎与Binance相当。

Upbit & Bithumb

Upbit 和 Bithumb 是韩国两大领先的加密货币交易所,表现总体比较突出。 Upbit在全球交易所中一直保持较高排名。Bithumb 作为韩国成立最早的交易所之一,在部分代币上表现十分优秀。韩国市场极高的炒币热情使大量资本涌入本土交易所,带来了较高的流动性与交易量。由于流动性深度较高,且韩国散户众多资金分散,使得价格变化在中长期尺度上不会太明显。然而,聚焦更短期的小时内交易,韩国所的交易量和价格波动均超出其他同层次交易所。由于本研究主要研究于代币上市后1天、7天和30天的价格变化情况,可能未能充分体现韩国交易所的突出表现。

值得注意的是,Upbit 和 Bithumb 有明显的“泡菜溢价”地区优势。某些代币在韩国交易所上市后,短期内价格通常会比全球其他交易所高出一定比例,这为Upbit和Bithumb带来了全球其他交易所无法比拟的优势。

Bybit

作为顶级交易所之一,拥有强大的流动性深度和丰富的上币经验,能够提供稳定的交易环境。尽管 Bybit 在 2025 年初经历了较大规模的盗币事件,但凭借其及时有效的公关处理和安全措施,展现了作为大交易所的应对能力。相比之下,许多小型交易所往往缺乏应对此类挑战的能力。Bybit 在风险管控和公关处理方面的应对策略也十分得当,尤其在财务资金方面保持充足,迅速恢复了用户的信任,并继续保持其在市场中的竞争力。

Bitget

在中型交易所中表现尤为突出,发展速度较快。Bitget 正处于向一线交易所进发的转型阶段,倾向于实施更为严格的上币机制。平台上线了较多新币,为投资者提供了更广泛的选择。同时,根据数据平均来看,已上线代币整体表现较好,并且币种的正向价格波动表现远超同层次平台。优质项目对Bitget的偏好逐步显现,平台在项目筛选上保持审慎,通过双向激励机制实现了更为精准的优中选优。整体而言,Bitget的市场表现介于顶级交易所和中型交易所的平均水平之间。展现了良好的价格表现和市场认可度。与同级交易所相比,Bitget上的代币价格波动较为平稳,在市场波动时表现出高度的韧性,从而维持了较强的市场竞争力和用户信任。

Gate

正在迅速崛起。凭借其上币数量的较高占比与不断创新的上币策略,Gate在2024年的数据表现比较出色,不仅交易量逐步攀升,代币涨幅也较为明显。Gate成功吸引了大量新兴项目,显著提升了市场竞争力,并不断扩大其在加密市场中的影响力。Gate 在 Meme 赛道上表现突出,同时设立了创新区,为新上线代币提供专属板块。凭借敏锐的市场洞察力,成功推出多个热门代币,吸引了大量投资者。其创新的上币策略和精准的项目筛选帮助平台快速扩展生态,提升了用户粘性,促进了交易量和流动性的增长。

KuCoin

在本报告重点研究的上币之外,KuCoin在合规性方面取得显著进展,KuCoin已与美国司法部(DOJ)达成和解,此结果为KuCoin及其新领导团队的未来发展铺平了道路。KuCoin也在积极获取相关牌照,尤其是在澳大利亚、印度,而在欧洲、土耳其等地,也在积极布局。KuCoin通过KuCoin EU Exchange GmbH在奥地利申请符合《加密资产市场法规》(MiCAR)的牌照。同时,KuCoin也是印度首个符合金融情报机构(FIU)规定的全球加密货币交易平台。通过推动合规性和区域扩展,KuCoin有望吸引更多潜在用户,促进交易量和价格增长,为其未来的持续增长创造了有利条件。

Coinbase & Kraken

作为美国最大的交易所,具备强大的流动性和深度市场。Coinbase的谨慎上币策略叠加美国较严格的加密货币监管政策,导致平台上币数量相对较少,但也具有较高的安全性与稳定性。说明Coinbase对待新项目,尤其是Meme币等高风险资产,采取了保守的上线策略。但是从价格表现上来看,在选择追求稳定,长远的发展同时,也错过了较多的上涨机会。Karken因其安全性而闻名,并受严格监管导致产品服务相对其他交易所较少。

6. 参考资料

1. Animoca Brands Research on 2024 Listing Report

https://research.animocabrands.com/post/cm71o17u2t6f107mlc6v09ujq

2. Low Float & High FDV: How Did We Get Here?

https://www.binance.com/en/research/analysis/low-float-and-high-FDV-how-did-we-get-here

3. CoinGecko2024 Annual Crypto Industry Report

https://www.coingecko.com/research/publications/2024-annual-crypto-report

4.국내 코인 거래소 총 투자자 1천500만명 첫 돌파…11월 60만명↑

https://www.yna.co.kr/view/AKR20241224079900002

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。