Author: Matti

Translation: Luffy, Foresight News

This is a story woven from myths, legends, and historical analogies, rather than starting from fundamental principles. Throughout my writing process, I have applied René Girard's scapegoat theory to the cryptocurrency field, and I suggest you familiarize yourself with his theoretical framework before diving deeper.

Rationality tells me that as the crypto industry matures, viewing the crypto space through a traditional cyclical lens has become outdated. However, deeply influenced by Girard's theory, I cannot escape the mythic patterns that keep emerging. When you have a hammer in hand, everything looks like a nail.

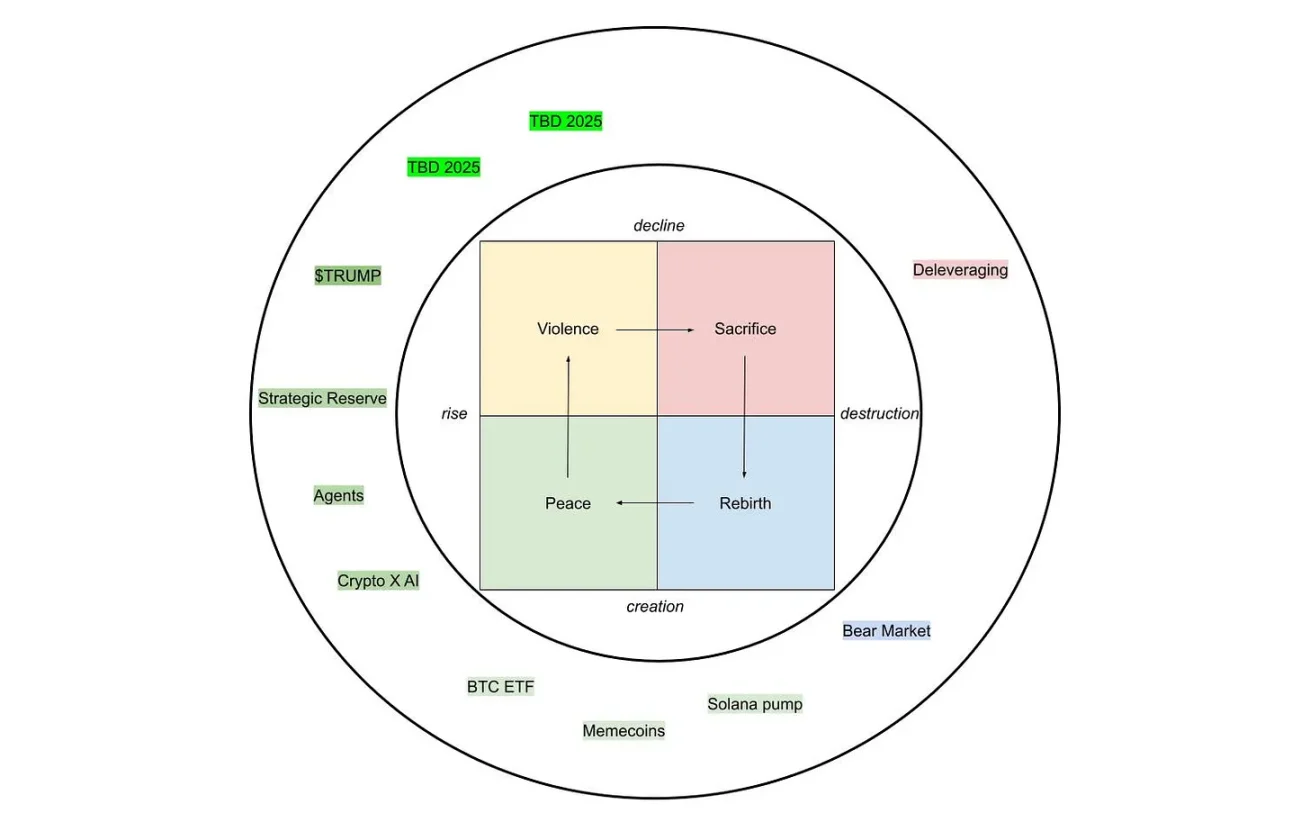

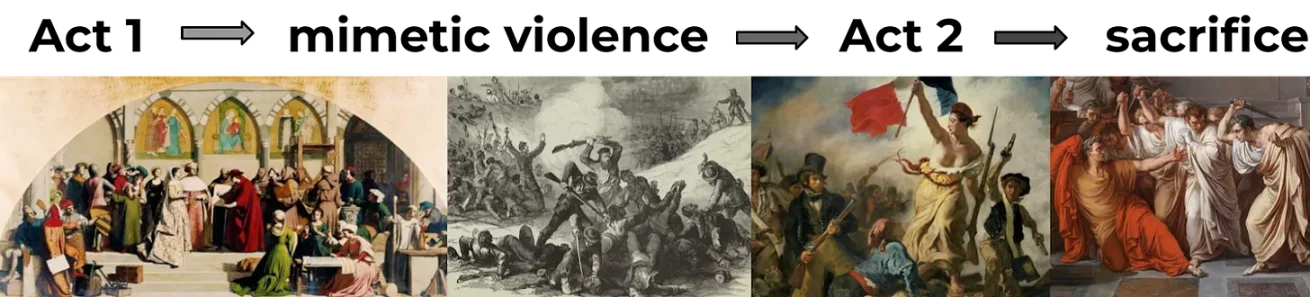

In this article, I will explore how the crypto bull market unfolds in two acts: the first act is preceded by an episode of "mimetic crisis," followed by the second act, which ultimately concludes with a "sacrificial crisis."

The first act begins with a price surge that ignites a mimetic desire throughout the community. The subsequent price crash triggers chaos and conflict, creating a symbolic "everyone is in danger" situation, where internal conflicts consume the entire crypto community.

The second act resolves the crisis of the first act through another price surge, thereby concluding the entire cycle and finding the ultimate scapegoat. Each cycle ends due to the overdevelopment of its fundamental principles, and each cycle has a scapegoat.

This reveals both a cyclical nature (which is not much different this time) and a linear development process (which is actually somewhat different this time). In the end, we always find ourselves in a new situation.

The collapse of Initial Coin Offerings (ICOs) left Ethereum in desolation, while the summer of decentralized finance (DeFi) allowed it to be reborn. The summer of DeFi raised doubts about whether Bitcoin could become a financialized asset, while Microstrategy and BlackRock restored confidence.

The bull market of 2017 was driven by ICOs, leading to an Ethereum bull market. Ethereum, the "world computer," turned into a slot machine. As ICO projects cashed out their raised Ethereum, this "computer" self-destructed, only to be revived by the DeFi craze in 2020, which ultimately ended with the collapse of over-leveraged speculators (such as Three Arrows Capital and SBF). The scapegoat of 2017 was not so individualized, but it was real.

In 2017, Ethereum's ICO projects were both the source of prosperity and the cause of decline; in 2021, the heroes of the summer of DeFi experienced the same journey. The best scapegoats are those who initially brought wealth and revelry, such as the wealth generated by Ethereum ICOs or the crazy lending and token issuance of DeFi, where participants could become millionaires just by participating, but ultimately became the cause of decline.

Bubbles are a side effect of imitation

The bull markets of 2017 and 2021 are clearly divided into two acts, and there is a striking similarity: both summers saw significant price declines. These episodes (brief but intense periods of decline) interrupted the initial price momentum, yet in the second act, driven by new market leaders, this momentum reignited with the same enthusiasm.

Escalation of Mimetic Conflict

During these episodes, as no scapegoat has yet appeared, mimetic conflict turns inward. Those familiar with Girard's theory know that this "everyone is in danger" chaotic situation is unsustainable; the search for a scapegoat will later serve as a purifying mechanism. But before that, conflicts will continue to escalate.

In 2017, the boom of ICOs and Bitcoin's scaling dilemma triggered a price crash in early summer: Bitcoin fell from $2,700 to below $2,000, and Ethereum dropped from $400 to $150, leading to collective conflict. The SegWit debate caused divisions among Bitcoin community members over block size, while the fork of Bitcoin Cash (BCH) further deepened this split.

When the Ethereum ICO bubble burst, users and developers blamed each other, and the Ethereum Foundation was accused of being the root cause of network congestion and fraud. The conflict between Ethereum Classic (ETC) and Ethereum (ETH) erupted, with ETC promoting a "pure" vision, skyrocketing tenfold from June to August, while fee disputes between miners and users further divided the community.

In 2021, a similar pattern emerged after the price crash in May. Bitcoin fell from $64,000 to $30,000, and Ethereum dropped from over $4,000 to $1,700, triggered by Elon Musk's criticism of Bitcoin and regulatory crackdowns in China.

Conflicts erupted in a more complex situation: Ethereum's gas fee issues sparked debates about scaling between L1 and L2 camps; the Bitcoin Mining Council caused divisions between purists and pragmatists; the collapse of DeFi liquidity mining projects (like Iron Finance) pitted speculators against each other; and negative rumors about Tether intensified competition among stablecoins.

The Second Act

From Girard's theoretical perspective, these episodes are turning points: the dominant participants in the first act collapse due to unsustainable over-prosperity, triggering internal conflicts, until the second act redirects people's desires toward new assets, thereby postponing the final sacrificial crisis.

In 2017, the first act was dominated by Ethereum and ICO projects. By June, driven by token sales like Bancor and Tezos, Ethereum's price soared from $8 to $400, while Bitcoin lagged behind. In the second act following the episode, fueled by retail investors' FOMO, Bitcoin's price surged to $20,000, with Bitcoin Cash (peaking at $4,000) and the so-called "Ethereum killer" EOS also joining the rally.

The first act belonged to Ethereum and ICOs; the second act was dominated by Bitcoin.

In 2021, the main characters of the first act were Bitcoin, Ethereum, and DeFi blue-chip projects like Aave and Uniswap, which gradually evolved into "institutional-grade" assets. In the second act following the episode, market attention shifted to the rapid rise of LUNA, the staking craze of OlympusDAO (3,3), and Solana reaching a peak of $260, with Avalanche (AVAX), Polkadot (DOT), and meme tokens (DOGE, SHIB) also riding the wave.

The first act belonged to Bitcoin, Ethereum, and DeFi blue-chip projects; the second act belonged to LUNA, OlympusDAO fork projects, Solana, and the broader altcoin rally.

Original Sin

Unlike the technological innovations represented by the ICOs of 2017 and the DeFi of 2021, the fundamental driving force of this cycle is institutional adoption. This is a top-down shift driven by Bitcoin spot exchange-traded funds (ETFs) and MicroStrategy's funding. However, all cycles share a common thread of financial engineering: global capital collaboration in 2017, on-chain yields in 2020, and institutional access in 2024.

While the chase for meme tokens may distract observers, it is merely a bait, much like non-fungible tokens (NFTs) in the previous cycle. This is a small cycle within a larger cycle. But it plays a crucial role in revealing people's rejection of grand ambitions: price becomes both a means and an end, a last-ditch effort to escape the predicament before institutions fully take control and fraud becomes the exclusive domain of white-collar workers.

Institutions have entered the game. This is no longer an empty talk of the Enterprise Ethereum Alliance in 2017, but a reality in 2024, with Bitcoin spot ETFs launching on January 11. Donald Trump’s election as president, promising to make the U.S. a crypto superpower, marks a significant step forward for cryptocurrencies. By November 2024, the crypto market is in a frenzy, with Wall Street entering the fray, strategic reserves seemingly on the horizon, and a stablecoin bill hinting at a new form of dollarization.

But Trump's inauguration in January 2025 brings anxiety. Amid negative rumors of trade wars and macroeconomic turmoil, expectations that the government would intervene in the market like a deity are dashed. The crypto community realizes that Trump, as a top influencer, has destroyed the market with his own meme token, abruptly ending the super cycle of meme tokens. The first act thus concludes, with the community looking to institutions for salvation, but the scapegoat is still nowhere to be seen.

Before the Second Act, the Bottom Has Not Yet Arrived

Now it is March 2025, and we are in the episode phase of the first act, with Bitcoin's price falling from its peak and the entire altcoin market suffering severe blows. The reason this episode phase may spiral out of control is that people genuinely believe everything is over. Conflicts escalate, and the community falls into chaos, but the scapegoat has still not appeared.

History suggests that the second act often triggers a frenzied price surge, redirecting people's desires and postponing the arrival of the sacrificial crisis. However, this does not mean that prices will necessarily skyrocket. The question is, when the overdevelopment of institutional adoption ultimately becomes unsustainable, who will we blame?

The scapegoat will inevitably come from those institutions that brought hope to this cycle. Will it be a vague, collective outcry — "institutions have strangled the crypto market" — pointing fingers at BlackRock's ETF empire, or those anonymous suits who have dollarized our resistance?

Or will it materialize into a more specific, personalized target? Will MicroStrategy collapse, its $40 billion Bitcoin bet evaporating in a spectacular leverage crash, making Michael Saylor the ultimate speculative king — once hailed as a visionary, now a scapegoat for our mistakes? Perhaps even our top KOL Trump, who has been hyping meme tokens, will become the target of blame.

This is not the bottom yet, at least not now. The mimetic chaos continues, and the second act is about to arrive. Whether it will first bring a frenzied surge like in the past, only to plunge into a deeper abyss, remains to be seen.

One thing is certain: the scapegoat is about to appear, and it may be dressed in a suit. If it is not in a suit, it may be blamed for that.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。