全球第二大稳定币 USDC 的发行商 Circle 正式启动上市计划,准备在纽约证券交易所挂牌。4 月 2 日,该公司向 SEC 提交了招股书,迈出了期待已久的 IPO 第一步。S-1 文件没有明确 IPO 时间表,但通常公司提交 S-1 后几周内即可开始交易。根据S-1 招股说明书,摩根大通和花旗将担任主承销商,市场预计 Circle 估值可能达到 50 亿美元,股票代码为「CRCL」。招股书显示,Circle 将发行未明确数量的 A 类普通股,同时现有股东也将登记出售部分持股。目前每股定价区间尚未确定。公司出售股份所得将归 Circle 所有,而现有股东售股所得不纳入公司。

这是 Circle 第二次尝试上市。2022 年底,它曾试图通过与一家 SPAC(特殊目的收购公司)合并的方式登陆资本市场,但因监管问题最终告吹,损失了超过 4400 万美元。此后,Circle 调整策略,逐步向金融中心靠拢。去年,它把总部从波士顿搬到了纽约世贸中心一号楼,进一步融入全球金融核心圈。

这一次,Circle 选择了一个微妙的时机——科技股近期波动剧烈,纳斯达克指数刚刚经历了 2022 年以来最惨淡的一个季度。如果成功上市,Circle 将成为继 Coinbase 之后,又一家登陆美国主流交易所的重量级加密货币公司,同时也是第一家稳定币上市公司。

利润持续承压的生态闭环

Circle 的故事始于 2013 年,当时它的定位是一家专注于比特币相关业务的公司,目标是通过技术让数字货币使用更加便捷。随着加密市场风云变幻,Circle 在 2018 年抓住了新的风口——与 Coinbase 合作,通过 Centre 联盟推出了美元稳定币 USDC。USDC 是一种与美元 1:1 挂钩的数字资产,旨在为加密交易提供稳定性和可信度。

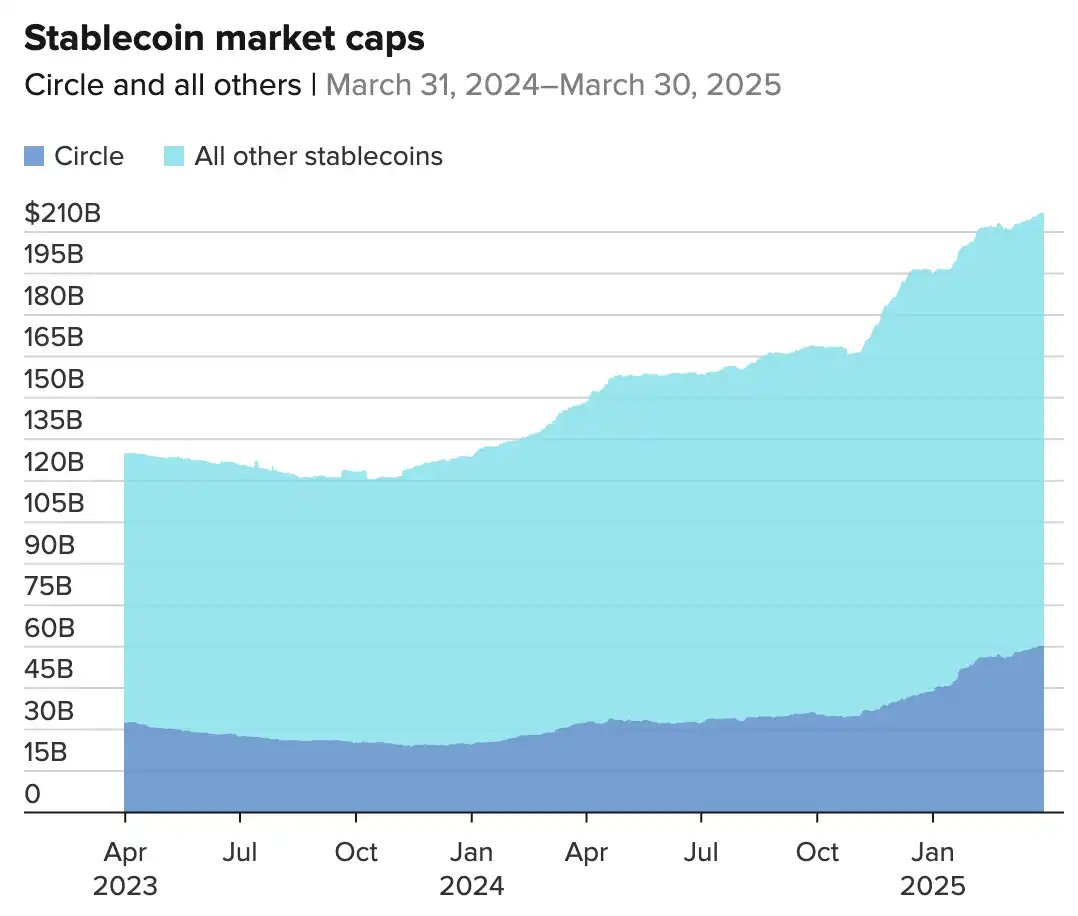

2023 年,Centre 联盟解散,Circle 获得了 USDC 的完全控制权。从此,USDC 不再只是一个合作项目,而是 Circle 的核心资产。截至 2025 年,USDC 的市值已达到 601 亿美元,虽然仍落后于 Tether 的 USDT(市值 1444 亿美元),但其增长势头和透明度让它在市场上占据了一席之地。

USDC 是 Circle 最知名的产品,这是全球第二大稳定币。USDC 在上一轮加密牛市中迅速崛起,市值从 2020 年的不到 10 亿美元飙升至 2022 年的超 500 亿美元,2024 年进一步增长至 601 亿美元,占整个稳定币市场的 26%。尽管龙头 Tether(USDT)仍以 67% 的市占率遥遥领先,但 USDC 今年增长迅猛——市值增长了 36%,而 Tether 只有 5%。

数据来源: CryptoQuant

相关阅读:《Circle IPO 冲刺 50 亿美元估值,稳定币有概念股了?》

渠道分销成本过高,毛利率持续下降

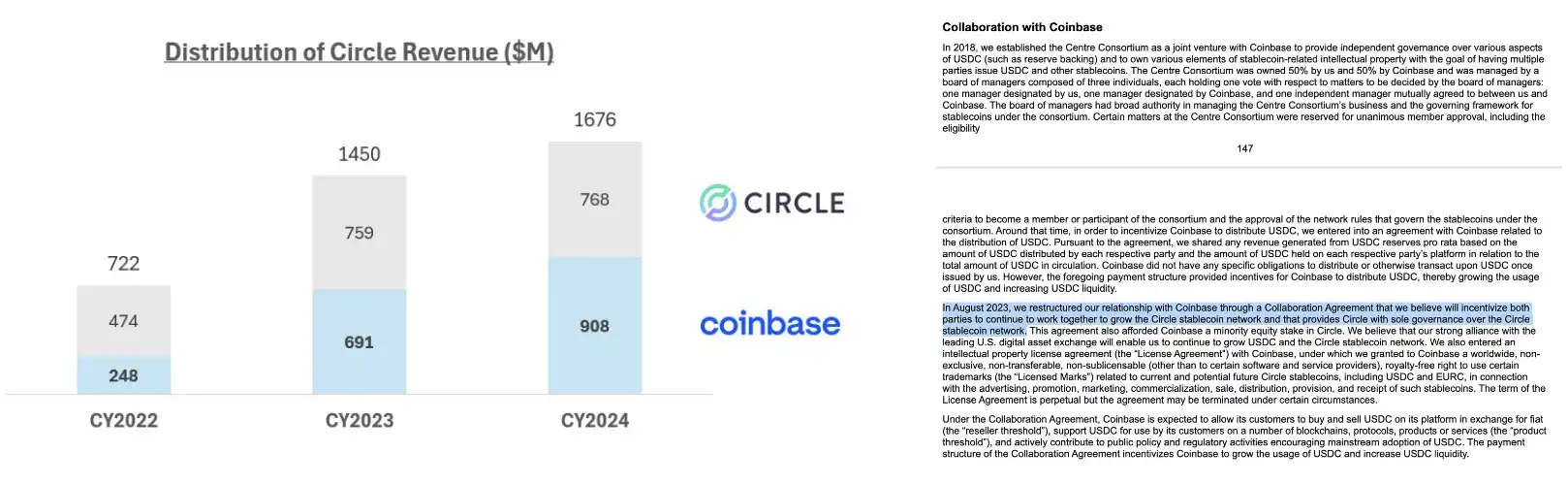

Circle 深知 USDC 的成功离不开生态支持。最初,它与 Coinbase 通过 Centre 联盟共同发行 USDC,但 2023 年联盟解散,Circle 全权接管。S-1 披露,Coinbase 如今持有 Circle 少数股权,双方基于储备总收入更平均地分配利润(仍按各自钱包和托管产品中的 USDC 持有量划分)。Circle 在 2024 年赚取了约 17 亿美元的收入,并作为分销合作伙伴向 Coinbase 支付了超 9 亿美元。

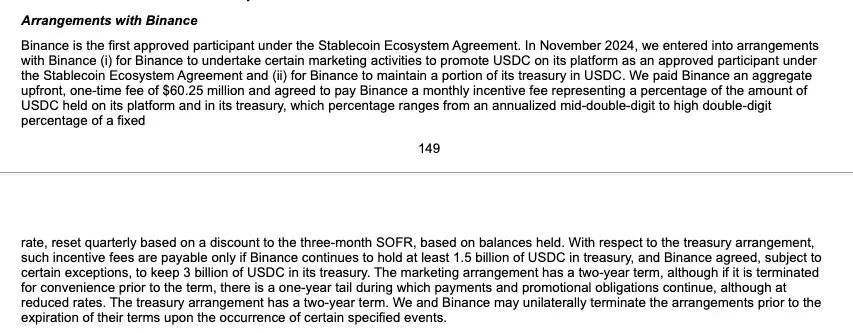

2023 年 12 月,Circle 又与全球最大加密交易所币安达成合作,支付 6025 万美元一次性费用,并按月支付一定比例费用,允许 USDC 参与 Binance Launchpool,促使 Binance 平台内 USDC 供应从不到 10 亿美元升至 40 亿美元。

这种「花钱买增长」的策略显著提升了 USDC 的流通量和市场认可度,但也增加了运营成本。Circle 通过与 Coinbase、币安、贝莱德等巨头的合作,构建了一个强大的分销网络,确保 USDC 在全球加密生态中的渗透力。

机构关系网成主要护城河

Circle 的业务模式可以用「稳定币+生态扩展」来形容。它不仅是一个稳定币发行商,还试图通过一系列产品和服务,打造一个覆盖加密支付、跨链技术乃至企业解决方案的生态系统。

USDC 发行与流通是 Circle 的核心业务,也是其最重要的收入来源。每发行一枚 USDC,Circle 都会在银行存入等值的美元或高流动性资产作为储备,确保其价值稳定。用户可以使用 USDC 进行交易、支付或储值,而 Circle 则通过管理这些储备资产赚取收益。为了扩大 USDC 的流通范围,Circle 与 Coinbase、币安、贝莱德等金融和加密巨头建立了深度合作。例如,在与 Coinbase 的协议中,Circle 会根据 USDC 储备的每日净收益设定支付基数,扣除管理费后双方按比例分成。截至 2024 年,USDC 的流通量持续增长,尤其在去 DeFi 和跨境支付领域占据了重要地位。

在支付与企业服务方面,Circle 扮演着连接加密世界与传统商业的桥梁角色。它提供了一套完整的支付 API 和企业级工具,使商家能够轻松接受 USDC 支付并自动兑换为法币。这种服务模式类似于传统金融中的 PayPal,但专为加密经济优化。例如,电商平台可以集成 Circle 的 Checkout 服务,消费者用 USDC 付款后,Circle 会实时将加密货币转换为美元并结算给商家,大幅降低了企业涉足加密支付的门槛。

跨链技术和区块链基础设施是 Circle 构建的另一个关键壁垒。该公司开发的跨链桥让 USDC 能够在以太坊、Solana 等不同区块链之间自由流转,极大提升了稳定币的可用性。此外,招股书透露 Circle 正在研发 Layer 2 解决方案,旨在降低交易成本并提升效率,布局加密基础设施。

为了更直接触达终端用户,Circle 还推出了数字钱包服务。虽然目前规模有限,但能看出业务正从 B 端向 C 端延伸。

总结一下,Circle 的业务模式就像一个「稳定币驱动的生态闭环」:以 USDC 为核心,通过支付、技术和用户服务,将加密货币的潜力延伸到现实世界。它的野心不小,几乎涵盖了 CEX 之外的所有加密领域。

去年 16.8 亿美元营收从哪来?

根据招股说明书,此次披露的财务数据首次完整呈现了 Circle 近年业绩表现。

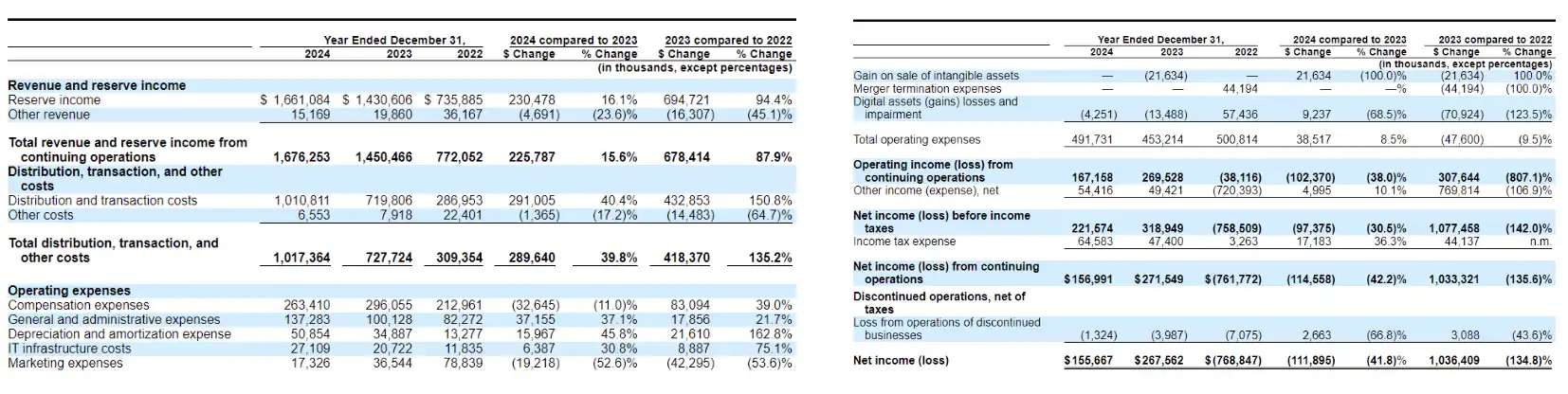

2023 财年(截至 12 月 31 日)总营收与储备收益达 16.8 亿美元,同比增长 16%,较 2022 年的 14.5 亿美元和 2021 年的 7.72 亿美元持续增长。2024 年收入主要来自支撑 USDC 的储备资产利息收益。

2024 年运营总支出 4.917 亿美元,其中薪酬支出(2.634 亿美元)、行政管理费用(1.373 亿美元)和 IT 基础设施投入(2710 万美元)占主要部分。持续经营业务净利润 1.569 亿美元,虽低于 2023 年的 2.715 亿美元,但较 2022 年 7.618 亿美元亏损显著改善。2024 年调整后 EBITDA 为 2.849 亿美元。

公司当年还录得 430 万美元数字资产减值损失,同时因非核心业务收益获得 5440 万美元其他收入。招股书暂未最终确定流通股加权平均数及每股收益数据。

根据规划,Circle 拟将 IPO 募集资金用于产品研发、运营资本、规模扩张及潜在收购等常规公司用途。目前尚未公布具体定价时间表与股份分配方案。

运营和财务指标

Circle 通过管理 USDC 的储备资产赚钱。这些储备包括现金和短期美国国债,在高利率环境下产生可观利息收入。S-1 显示,2024 年 Circle 总营收 16.8 亿美元,其中 99%(约 16.65 亿美元)来自储备收入,其他来源(如支付服务和跨链技术)仅贡献 1500 万美元。这意味着 Circle 几乎完全依赖单一收入来源,且受政府利率政策影响。文件估算,若利率下降 1%,储备收入将减少 4.41 亿美元。不过,Circle 认为低利率可能刺激 USDC 流通量增长,但这种关系「复杂、不确定且未经证实」。

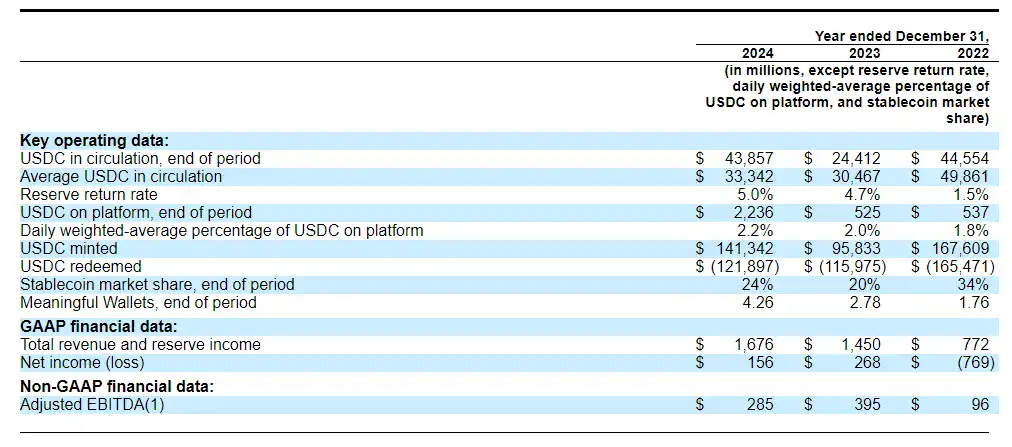

截至 2024 年 12 月 31 日,USDC 已用于约 20 万亿美元的链上交易。下表列示了在所述期间的关键运营和财务指标,以及相关的 GAAP(美国公认会计准则)度量标准:

USDC 流通量和平均 USDC 流通量是 Circle 储备收入的主要贡献因素,也是衡量 Circle 稳定币生态系统广度的指标。截至 2024 年 12 月 31 日、2023 年 12 月 31 日和 2022 年 12 月 31 日,公司持有的 USDC 分别为 2.945 亿美元、2.758 亿美元和 530 万美元。

储备回报率(Reserve Return Rate)是指储备资产所产生的回报率,是储备收入的主要决定因素,其计算方式为储备收入除以 Circle 稳定币持有者专属储备的平均期间余额。截至 2024 年 12 月 31 日、2023 年 12 月 31 日和 2022 年 12 月 31 日,公司储备回报率分别为 5.0%、4.7%和 1.5%。

稳定币市场份额(Stablecoin Market Share)指的是流通中的 Circle 稳定币占所有法币支持稳定币(即锚定法定货币价值的数字资产)总流通量的比例。该指标反映了 Circle 稳定币在整个稳定币市场中的占比及其在竞争格局中的地位。自 2021 年以来,按流通量计算,Circle 一直是全球第二大稳定币发行方。根据 CoinMarketCap 数据,截至 2024 年 12 月 31 日,Circle 的稳定币市场份额为 24%。

有效钱包(Meaningful Wallets)指的是链上 USDC 余额超过 10 美元的数字资产钱包数量,是衡量 USDC 采用广度的重要指标。2024 年有效钱包数量为 426 万个,较 2023 年底增长 53.24%。

利润拆解

下表为 Cirlce 公司 2024 年利润表,详细记录了公司 2024 年各项收入、费用及净利润指标:

截至 2024 年 12 月 31 日,储备收入为 16.76 亿美元,相比 2023 年同比增长 2.305 亿美元(16.1%)。其中,约 1.399 亿美元的增长来自于流通中 USDC 日均余额增长,这反映了与数字资产交易活动相关的 USDC 需求增加以及 Circle 在关键市场中的市场份额提升;8,990 万美元的增长来自平均收益率的提升,主要受美联储加息的影响。2024 年度其他收入同比下降 470 万美元(23.6%),主要原因是交易服务收入下降 390 万美元,这与 2024 年某些服务的逐步停用有关。

2024 年年度的分销和交易成本相较于 2023 年底增加了 2.91 亿美元(40.4%),主要原因是支付给 Coinbase 的分销成本增加了 2.166 亿美元,以及与新的战略分销伙伴关系相关的其他分销激励成本增加了 7,410 万美元,如向币安支付的预付一次性费用。2024 年度其他费用与 2023 年度相比减少了 140 万美元(17.2%),主要原因是公司停用传统交易服务产品,相关费用减少了 90 万美元。

2024 年年度利润为 1.56 亿美元,相较于 2023 年度净收益下降 1.12 亿美元。尽管 2024 年储备收入相比 2023 年同比增长 2.305 亿美元,但分销和交易成本相较于 2023 年底也大幅增加 2.91 亿美元,总营业费用增加 0.39 亿美元,最终导致利润呈现下滑态势。

在现金流方面,2022-2024 年连续三年,存放在银行账户中的 USDC 储备现金余额远远超过了每个金融机构 25 万美元的 FDIC 保险限额。截至 2024 年 12 月 31 日,约 85% 的 USDC 储备存放在 Circle 储备基金中,其余部分则以现金形式存放于若干银行账户中。Circle 储备基金由贝莱德管理。该基金仅对 Circle 可用,且 Circle 是 Circle 储备基金的唯一股东。

在融资方面,2024 年度,融资所得资金为 194.499 亿美元,而 2023 年度融资所得资金为 -203.222 亿美元,主要由于 2024 年流通中 USDC 增加,稳定币持有者存款净变化增加了 194.521 亿美元;而 2023 年流通中 USDC 减少,稳定币持有者存款净变化减少了 203.222 亿美元。

薪酬花费过高遭质疑,高管才是 IPO 的真正赢家?

Circle 的 IPO 不仅关乎公司未来,也是一场资本盛宴。Circle 上市后,将实行三级股权结构:IPO 发行的 A 类股每股 1 票投票权;联合创始人 Jeremy Allaire 与 Patrick Sean Neville 持有的 B 类股每股 5 票,但总投票权占比不超过 30%;C 类股无投票权,在特定条件下可转换。B 类股在非许可渠道转让时将自动转为 A 类股。

此外,根据招股书披露,高管薪酬 CEO Jeremy Allaire 年薪 90 万美元,股票奖励 900 万美元,外加 200 万美元福利,总薪酬超 1200 万美元。首席财务官 Jeremy Fox-Geen 总薪酬 520 万美元(年薪 50 万+股票 400 万+福利 70 万)。其他高管如首席战略官 Elisabeth Carpenter、总裁兼首席法务官 Heath Tarbert、首席产品和技术官 Nikhil Chandhok,年薪酬在 400 万-500 万美元之间。在 Circle 工作显然回报丰厚。

对于风投巨头来说,持有 5% 以上股份的投资者将大赚一笔,包括 General Catalyst(最大企业股东)、北京 IDG Capital、Breyer Capital、Accel、Oak Investment Partners 和 Fidelity。这些机构共持有超 1.3 亿股,估值 40 亿-50 亿美元的 IPO 将为他们带来可观回报。

USDC 市值在过去一年翻倍,从约 300 亿美元增至 600 亿美元,但市场竞争日益激烈。主要对手 Tether(USDT)以超 1400 亿美元的市值遥遥领先。此外,PayPal 于 2023 年推出自家稳定币,摩根大通等银行巨头也在探索区块链领域。S-1 文件中,Circle 列出了这些竞争者,坦言市场环境复杂。

尽管如此,Circle 对未来持乐观态度。美国针对稳定币的立法进程加速推进,其中《GENIUS 法案》和《STABLE 法案》备受瞩目。众议院数字资产小组委员会主席 Bryan Steil 表示,经过 4 月 2 日的审议,两法案有望在修订后实现一致,并计划在特朗普政府前 100 天内送交总统签署成法。这一进展为 Circle 等合规型稳定币企业提供了政策利好,也标志着美国在数字美元领域的监管框架日益清晰。

本次 IPO 仍需通过监管审查并视市场条件推进,具体发行规模、每股估值等细节将在上市前通过补充文件披露。虽然还存在一切不确定性,但 Circle 的 IPO 很可能会成为稳定币行业未来走向的一个关键信号。随着全球监管政策日趋明确,稳定币正迈向合规化和机构深度参与的时代。Circle 能否抓住这一机遇,借助华尔街为加密市场带来的充沛资金流,挑战 Tether 长期占据的王者宝座?在监管、竞争和市场波动的多重挑战下,Circle 能否兑现市场期待?这一切还需要时间来证明。

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。