Original text from Grayscale Research

Compiled by|Odaily Planet Daily Golem (@web3golem)_

Core Arguments:

Smart contract platforms are the core infrastructure for decentralized applications and blockchain-based finance. Therefore, they are central to the vision of public blockchains providing new frameworks for financial markets and digital trade.

Grayscale Research believes that the trend of application adoption of smart contracts will accelerate in the next 1-2 years, partly due to regulatory changes in the U.S. and upcoming legislation.

Based on market capitalization, the scale of the application ecosystem and developer community, as well as the value of on-chain assets, Ethereum is the largest smart contract platform. However, it has recently lagged behind some competitors, including Solana, in terms of fees (revenue) and other on-chain activity metrics.

Ethereum's differentiated characteristics emphasize a culture of decentralization, security, and neutrality, which will help it continue to attract a large number of users, developers, and transaction fees in the smart contract platform space, even as some newer blockchains capture market share. Therefore, ETH should be viewed as an important component of a diversified crypto portfolio.

The outlook for smart contract platform fees is highly uncertain, partly because we do not know how much pricing power platforms like Ethereum can maintain in the long term. However, in this report, Grayscale research indicates that Ethereum has the potential to increase total fees to over $20 billion (with an annualized growth of about $1.7 billion over the past six months) by executing its scaling strategy and maintaining pricing power.

Ethereum is still expected to capture a large share of on-chain activity in the future

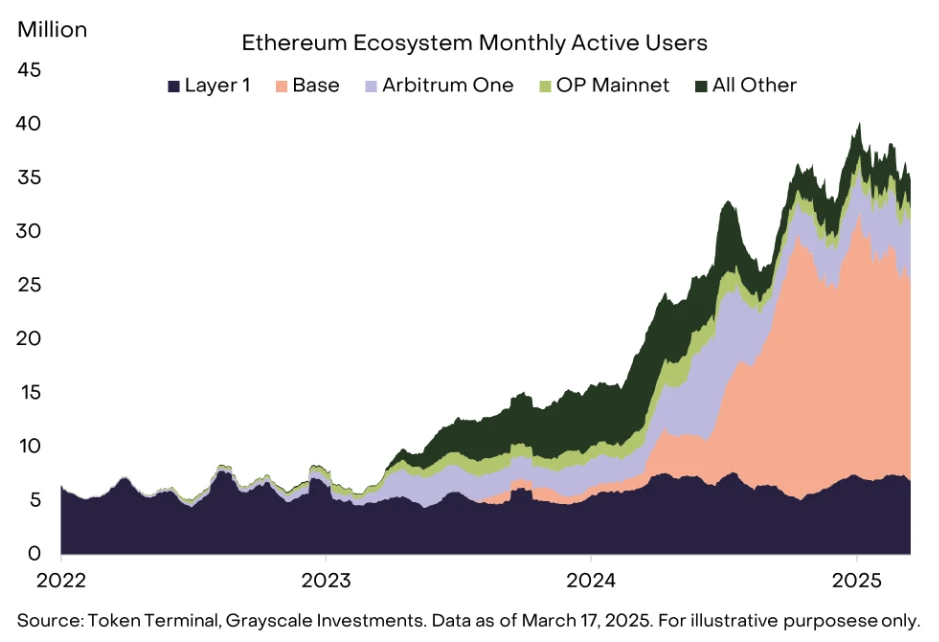

Similar to Linux, Python, and a few other examples, Ethereum is regarded as one of the most important open-source software projects in history. Despite being less than 10 years old, the current Ethereum network consists of over 11,000 nodes, processing 35 to 40 million transactions per month, with a value of approximately $46 billion, supported by over 2,100 full-time developers. The broader Ethereum ecosystem, composed of interconnected blockchains, can now handle about 400 million transactions per month.

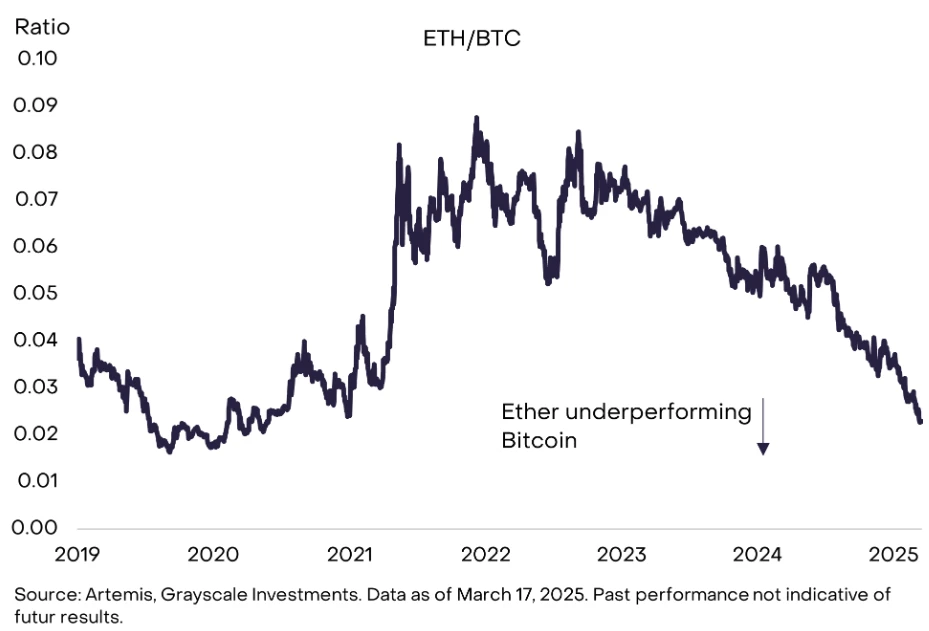

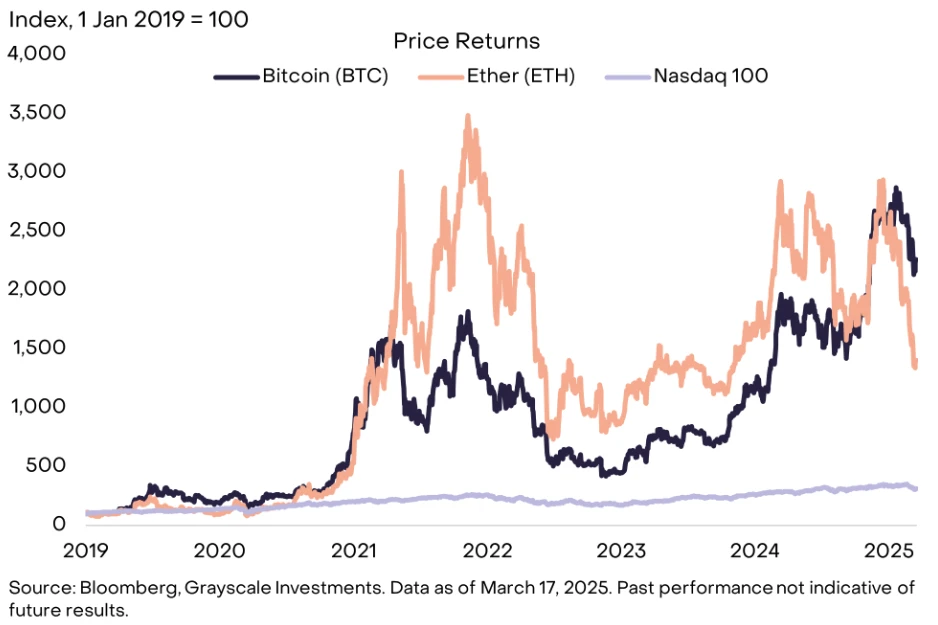

Despite its prominent position in the crypto industry and the launch of spot-based exchange-traded products (ETPs) last year, ETH's market capitalization significantly lags behind BTC. In fact, the ETH/BTC exchange rate has dropped to levels last seen in mid-2020. From a market capitalization perspective, since the end of 2022, ETH's market cap has grown by about $90 million, while BTC's market cap has increased by about $1.35 trillion (approximately 15 times). ETH's recent performance has also lagged behind some other smart contract platform tokens, such as Solana and Sui.

ETH has underperformed BTC for over 2 years

The continued underperformance has led some observers to question the future of Ethereum network activity and the value of ETH. While there is uncertainty about the prospects of every crypto asset, we continue to believe that ETH should be an important component of a diversified crypto portfolio.

Ethereum cannot be directly compared to Bitcoin. The Bitcoin network is a monetary system, with Bitcoin primarily used as a medium for value exchange and storage. In contrast, Ethereum is an application platform, with ETH providing utility for users of these applications. Although the prospects for smart contract technology are broad, we have yet to see widespread adoption of decentralized applications based on smart contracts. There are many early success stories (including the growth of stablecoin trading), but the current adoption rate remains low compared to the vision for smart contract platforms, which aim to bring most traditional finance on-chain.

Grayscale Research believes that the development of smart contract-based applications will accelerate in the next 1 to 2 years, partly due to regulatory changes in the U.S. and upcoming legislation. The Trump administration has made changes to federal crypto policy, allowing the industry to invest and thrive in the U.S. Additionally, a bipartisan group of senators has proposed the "Guidance and Establishment of a National Innovation for Stablecoins (GENIUS) Act," which builds on efforts from the last Congress to provide a comprehensive regulatory framework for the issuance of payment stablecoins. Clearer regulations should help increase investment and adoption of blockchain-based applications, thereby boosting on-chain activity (such as transactions and fees) and ultimately leading to value accumulation for smart contract platform tokens.

In addition to having a "first-mover advantage," Ethereum now faces competition from other smart contract platforms. However, Ethereum still possesses differentiating features that are particularly valuable for financial use cases, including a large amount of on-chain capital and a culture that emphasizes decentralization and neutrality. Therefore, we expect Ethereum to capture a significant share of future on-chain activity, which in turn will drive ETH prices up.

Ethereum - The World Computer

Ethereum is the first mainstream smart contract blockchain, and like Bitcoin, the Ethereum blockchain can also be used to send and receive transactions. However, with the increase in smart contracts, Ethereum can also run decentralized applications. These applications can be anything from decentralized lending platforms to identity solutions to video games. Because Ethereum serves as the infrastructure for applications, it is viewed as a software-based computer, sometimes referred to as the "world computer."

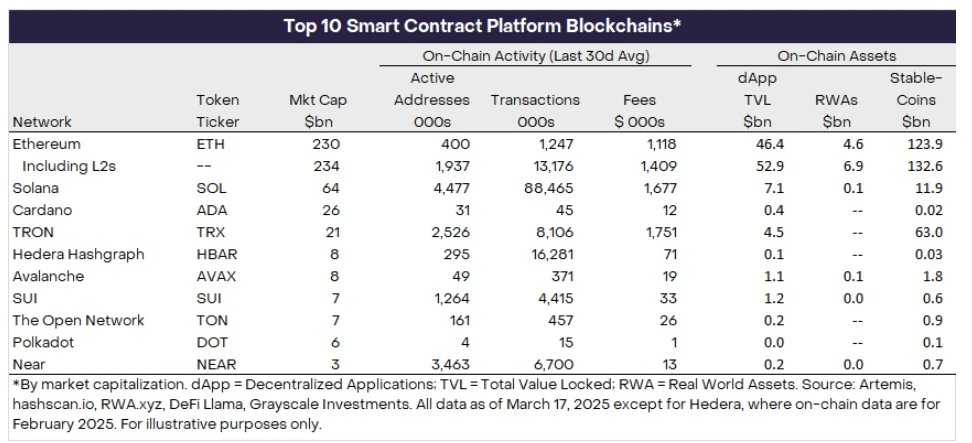

Today, there are thousands of applications on Ethereum, and compared to other smart contract blockchains, Ethereum has more on-chain assets (such as stablecoins and tokenized assets). However, it has recently lagged behind other blockchains in metrics such as on-chain activity. Solana is the second-largest network by market capitalization among smart contract platforms, with higher active addresses, transactions, and fees over the past 30 days, yet its market cap is only 30% of Ethereum's.

Top 10 Smart Contract Platforms

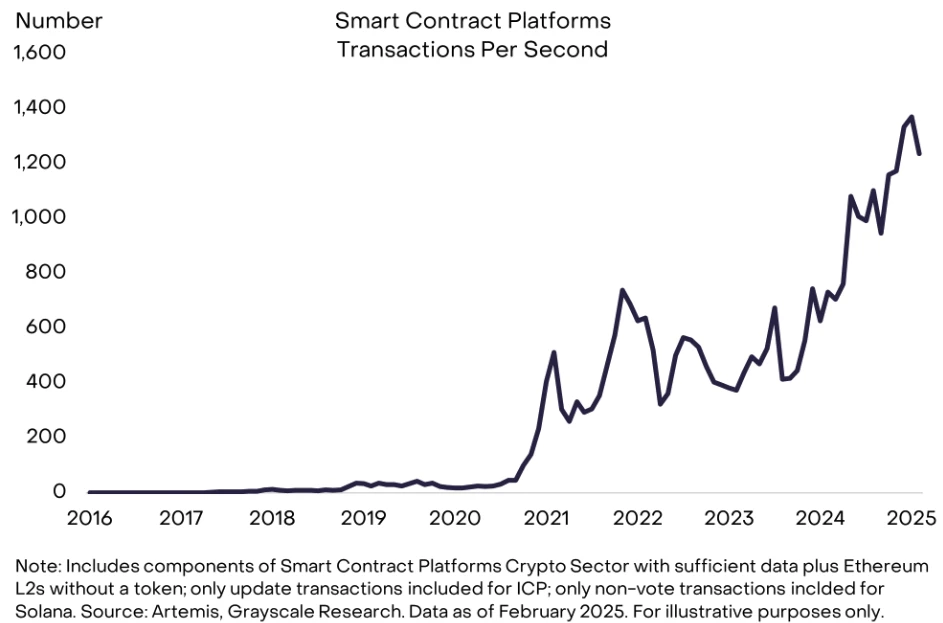

The investment logic for smart contract platforms is that new applications will bring more users and transactions, ultimately generating more fees for the underlying protocol. We estimate that the transaction volume of smart contract platforms has increased from about 20 transactions per second (TPS) five years ago to about 1,200 TPS today, with an annual growth rate of approximately 130%. In comparison, the Visa network processed about 7,400 TPS in the 12 months ending September 30, 2024. If smart contract blockchains can continue to grow in digital payments, establish competitive moats, and maintain pricing power, then fee revenue and token value could rise in the future.

Smart contract blockchains process ~1,200 transactions per second

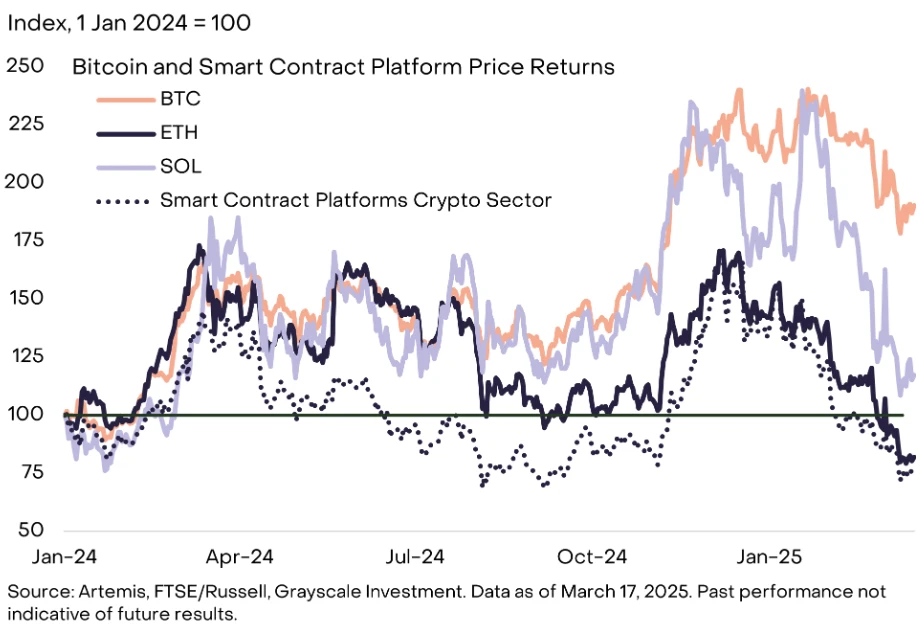

According to the FTSE/Grayscale Smart Contract Platform Crypto Industry Index, ETH's performance is roughly in line with its peers. The crypto smart contract space currently includes 70 tokens, with a total market capitalization of $428 billion. Since the beginning of 2024, the smart contract platform index has declined by 22%, while ETH's price has dropped by 18%. In contrast, Solana's price has risen by 18%, and Bitcoin's price has increased by 90%.

ETH's performance is roughly in line with the index

Ethereum Network Fees

Ethereum profits from network activity through transaction fees (known as "gas fees"), which are payments made by users when executing transactions or interacting with smart contracts. Unlike Solana and many other blockchains, activity in the Ethereum ecosystem occurs simultaneously on both the L1 Ethereum mainnet and L2 networks. This is how Ethereum intends to scale to millions of users, as L1 alone cannot adequately scale without sacrificing decentralization. If coordinated properly, this layered structure should provide users with high throughput and low L2 transaction costs while retaining the security and decentralization of L1.

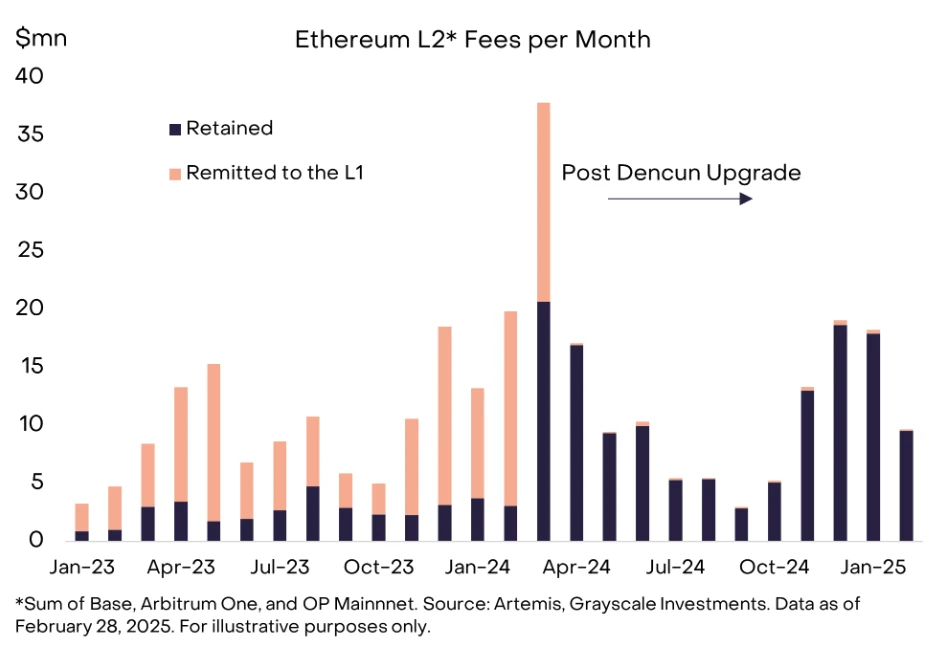

L2 networks like Arbitrum One and Base also charge transaction fees, and because they rely on the Ethereum L1 network for final settlement and security, L2s can charge lower transaction fees and process more transactions per second. However, L2s still remit a portion of fees to L1 as payment for settlement and security services. Last year, Ethereum underwent the Dencun upgrade, which introduced blob transactions, reducing the cost for L2s to publish their data to L1. This upgrade successfully increased the number of users and transactions on L2.

Significant growth in activity on Ethereum L2

However, the introduction of blob transactions has also affected the overall fee levels and distribution across the network. Blob transactions have reduced the fees that L2s pay to L1, leading some observers to view L2s as "parasitic" to Ethereum, as the short-term success of L2 comes at the expense of L1. However, if L2s benefit from the Ethereum ecosystem (such as security assurances and other network effects), then in the long run, a large L2 ecosystem will ultimately bring more value to the Ethereum network and ETH.

Ethereum L2 now pays lower fees to L1

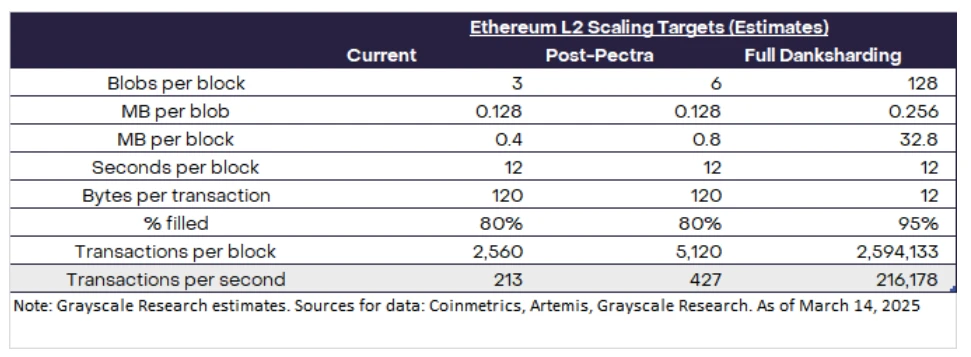

Future upgrades to Ethereum will continue to expand L1 and L2. The Pectra upgrade is scheduled for April 2025, combining Prague (execution layer) and Electra (consensus layer). To address scalability, Ethereum Improvement Proposal 7691 optimizes blob storage, aiming for 6 blobs per block, effectively doubling the blob capacity of Dencun. Looking ahead, Ethereum's scalability potential may significantly increase with the implementation of a concept known as Full Danksharding.

Future Ethereum upgrades will greatly increase L2 capacity

The Outlook for Ethereum Fees

The outlook for smart contract platform fees is highly uncertain, partly because the technology is in its early stages, and we do not know how much pricing power platforms like Ethereum can maintain over time. Smart contract platforms compete with each other while also competing with centralized systems; to maintain pricing power in the long term, they need to offer differentiated features to prevent users from migrating to cheaper (centralized or decentralized) systems. Although the Ethereum blockchain is slower and more expensive than many competitors, Grayscale Research believes its unique advantages (including high-value on-chain assets and an emphasis on decentralization and security) will contribute to its adoption and network effects, ultimately providing Ethereum with a certain degree of pricing power.

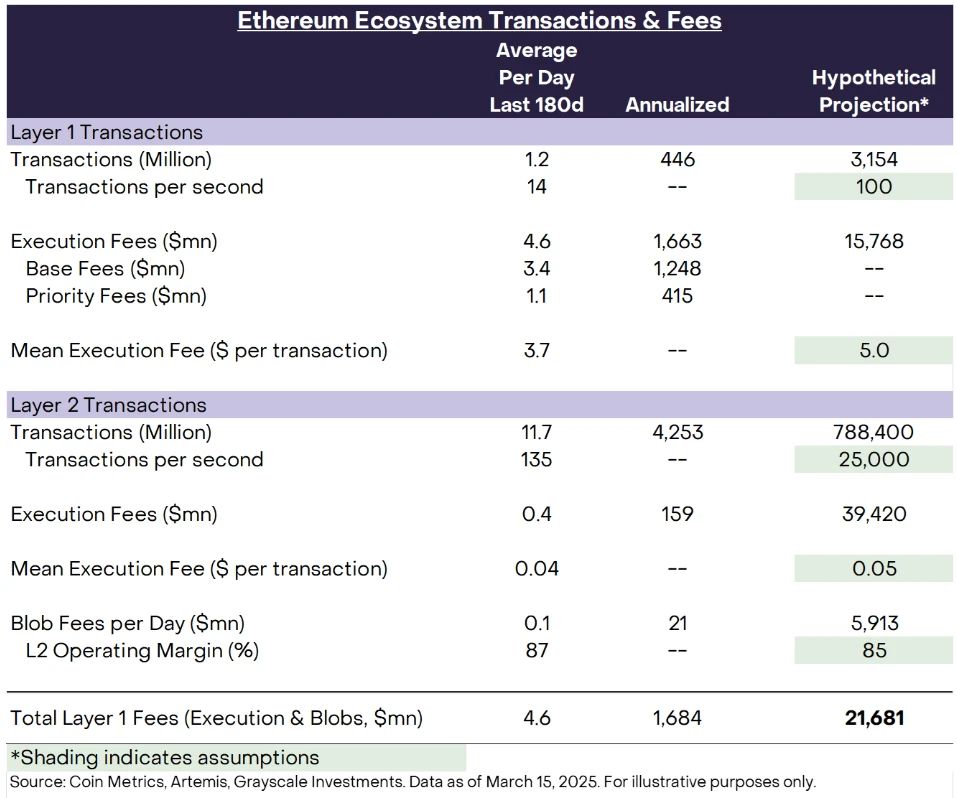

The following chart illustrates how Ethereum can increase fees by increasing capacity and maintaining pricing power. We assume an average transaction fee of $5 for L1, while the average fee since 2019 has been $6.3. In the long run, L1 will likely be used mainly for high-value transactions and those requiring high security assumptions, while for L2, we assume an average transaction fee of $0.05. If we further assume that Ethereum L1 can handle 100 TPS and that Ethereum L2 can collectively handle 25,000 TPS, these assumptions can be realized within the next 3 to 5 years under Ethereum's scaling roadmap.

Ethereum fee revenue can grow with increased capacity and pricing power

Under these assumptions, the total fees for Ethereum L1 will grow to $20 billion, although the annualized growth rate over the past six months has been about $1.7 billion. Despite the highly uncertain fee outlook, if Ethereum executes its scaling strategy and maintains a certain level of pricing power, it should theoretically be able to significantly increase fee revenue. To track progress, investors should consider monitoring the fundamental variables in this simplified model, namely L1 and L2 TPS, as well as average execution fees for L1 and L2.

First, make the pie bigger

In the last crypto bull market, BTC and ETH appreciated almost in sync, and even in 2021, ETH's price rose faster, ultimately peaking in November 2021, with a price return approximately twice that of Bitcoin. Some cryptocurrency investors may expect the same to happen in the current cycle, with ETH's performance clearly outperforming other tokens as the cycle matures, although recent results have been disappointing.

In the last crypto cycle, ETH ultimately outperformed Bitcoin

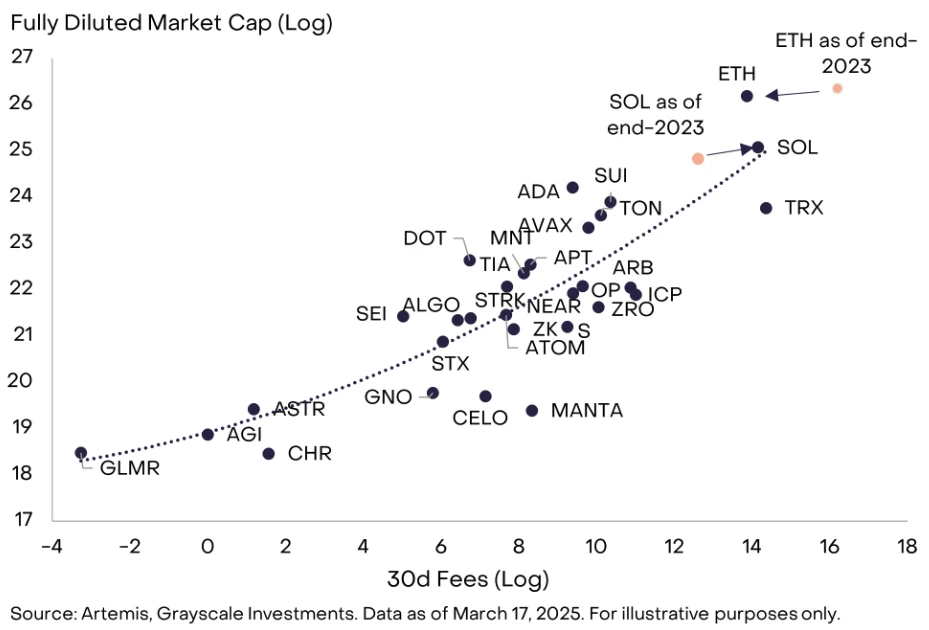

However, Grayscale Research believes that ETH's underperformance precisely indicates that the crypto market is still focused on fundamentals, which is a healthy sign. In Grayscale's analytical framework, the crypto market primarily distinguishes the value of smart contract platforms based on fees. Although fees do not translate into token value accumulation in exactly the same way on the blockchain, they are generally passed on to token holders, and fees can be considered the most directly comparable measure of blockchain activity.

In the realm of smart contract platforms, both Ethereum and Solana have relatively high fees and market capitalizations. Since the end of 2023, Solana has seen an increase in fee revenue and market share in the smart contract platform space, while Ethereum has lost its primary position in fee revenue and market capitalization. In other words, due to changes in fundamentals, the market has appropriately repriced the relative values of Ethereum and Solana. As shown in the chart below, Solana has moved up and to the right, while Ethereum has moved down and to the left, indicating that today's valuation may be higher than its fee revenue.

Due to weak fee growth, ETH has underperformed Solana

These small differences in competitive positioning are important, but they are not as significant as the potential growth of the entire category, as the adoption of all smart contract platforms is still in its early stages. For example, today Ethereum has only about 7 million monthly active users, while Meta Platforms, the parent company of Facebook, reported 3.35 billion "daily active users" in December 2024.

As adoption rates increase, smart contract platforms are expected to benefit from compound network effects, which can drive higher transaction volumes and fee revenues, as well as accelerate developer activity, liquidity depth, and cross-ecosystem interoperability. This reinforcement of adoption and utility may amplify the value capture capabilities of the entire sector.

Ultimately, the networks that win in competition may be those that collect the most transaction fees over time and have favorable structural supply and demand conditions for their native tokens. Solana, SUI, and several other smart contract platforms will share characteristics of high throughput, low transaction costs, and good user experience. However, what sets Ethereum apart is its large and diverse ecosystem of applications and developers, substantial on-chain capital, and a culture that prioritizes decentralization, security, and neutrality. We expect these features to continue attracting many users to the Ethereum ecosystem, and Ethereum will capture a significant share of economic activity on future smart contract platform blockchains.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。