Please note that VanEck has exposure to bitcoin.

Three key takeaways for mid-February – mid-March:

- Key Data Threatens Bull Market: Bitcoin’s 30% retracement coincides with historically low futures funding rates and the longest ETF outflow streak since inception. Altcoins remain weak while Bitcoin (BTC) dominance holds steady, reflecting abnormally weak bull market demand for speculative blockchain use cases.

- Corporate Bitcoin Yield Strategies Scale : MSTR, Metaplanet, and SMLR continue expanding BTC-backed financial engineering, with MSTR acquiring 20,356 BTC ($1.99 billion) and launching a $2 billion convertible note. The new REX Shares Bitcoin Convertible Bond ETF highlights the growing institutional interest in BTC treasuries.

- Texas Energy Bills Could Reshape Mining Economics : SB6 could raise interconnection costs and delays for large miners, while SB1942 would fast-track ERCOT approvals for flexible loads, creating a competitive edge for miners that generate their own power on-site. SB388’s 50% dispatchable energy mandate may drive up long-term mining costs by shifting Texas’ power mix toward fossil fuels.

- Chart of The Month

- Monthly Dashboard

- Bitcoin’s Network Activity, Adoption, and Fees

- Regulatory and Geopolitical Developments

- Bitcoin on Balance Sheets and Enterprise Value Analysis

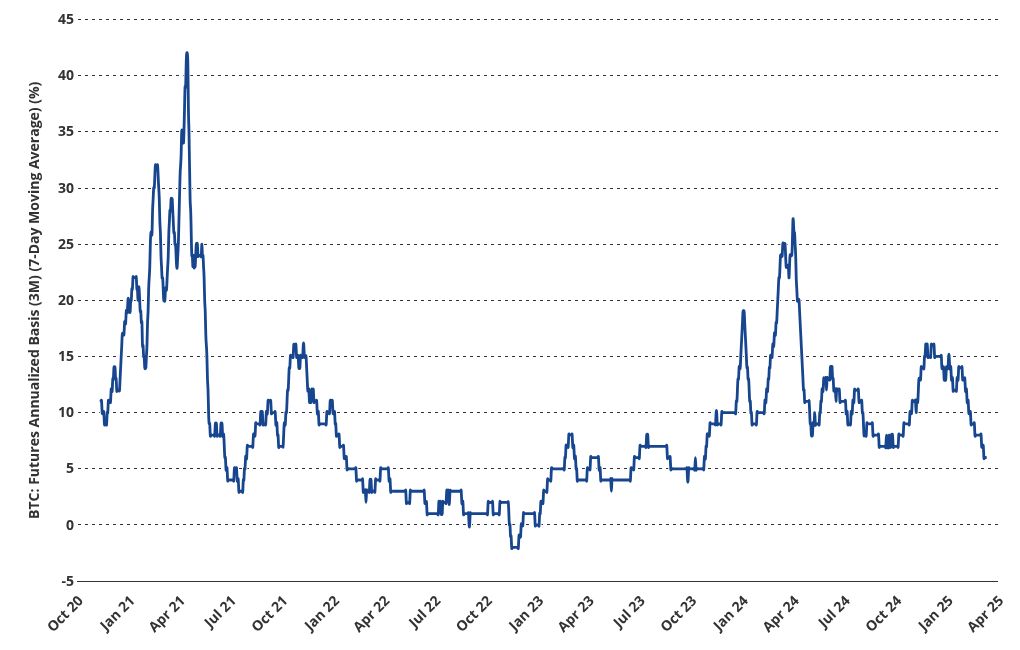

Chart of the Month: A Collapse in Animal Spirits?

3-Month Futures Roll Yield Hits Multi-Year Lows as Hedge Funds Exit Basis Trade

Source: Glassnode as of 3/13/202. Past performance is no guarantee of future results.

One of the most striking market sentiment indicators this month is the sharp decline in Bitcoin's funding rate, which has reached its lowest level since October 2023. The funding rate reflects the cost of borrowing to go long BTC in perpetual futures contracts. When it falls to such lows, it signals a cooling of speculative enthusiasm—what some might call a lack of “animal spirits” in the market.

This decline suggests that hedge funds have largely closed out the basis trade, a common strategy where traders arbitrage the spread between spot and futures prices. While some of this may be attributed to tighter futures spreads following the U.S. spot Bitcoin ETF launch, broader macro uncertainty and risk management adjustments could also play a role. With lower borrowing costs, this is the lowest speculative positioning in over a year, reminiscent of the pre-ETF environment when investors were still waiting on a catalyst for renewed bullish momentum.

However, while speculative fervor has clearly waned, this is far from the capitulation levels seen in the bear market depths. While the funding rate remains low, it has not flipped negative, which would indicate rare bearish periods of aggressive shorting. Instead, the market appears to be resetting expectations after the Trump trade as investors await a new catalyst to rekindle risk appetite.

Bitcoin Monthly Dashboard

| As of March 17th, 2025 | 30-day avg | 30 day change (%) 1 | 365 day change (%) | Last 30 days Percentile vs all-time history (%) |

| Bitcoin Price | $88,967 | -12 | 46 | 98 |

| Daily Active Addresses | 741,594 | -3 | -21 | 67 |

| Daily New Addresses | 309,731 | -3 | -25 | 56 |

| Daily Transactions | 399,582 | 9 | 7 | 91 |

| Daily Inscriptions | 140,976 | 62 | 13 | 53 |

| Total Transfer Volume (USD) | $63,167,619,258 | -5 | -1 | 87 |

| Supply Active, last 180 days | 26% | 2 | 46 | 45 |

| % Supply Dormant for 3+ Years | 45% | 0 | 1 | 64 |

| Avg Fees (USD) | $1.42 | -14 | -80 | 64 |

| Avg Fees (BTC) | 0.00002 | -2 | -86 | 4 |

| Percent of BTC Addresses in profit | 90% | -7 | -7 | 74 |

| Unrealized profit/loss ratio | 0.51 | -11 | -15 | 70 |

| Global Power Consumption (TWh) | 155 | 1 | 40 | 100 |

| Total Daily BTC Miner Revenues (USD) | $40,538,898 | -20 | -30 | 90 |

| Total Crypto Equities' Market Cap * (USD) (MM) | $181,909 | -19 | 52 | 81 |

| Transfer volume from Miners to Exchanges (USD) | $5,034,007 | -16 | -42 | 84 |

| Bitcoin Dominance | 60% | 3 | 16 | 90 |

| Bitcoin Futures Annualized Basis | 7% | -38 | -50 | 3 |

| Mining Difficulty (T) | 111 | 1 | 37 | 100 |

* DAPP market cap as a proxy, as of March 14th, 2025.

1 30 day change & 365 day change are relative to the 30-day avg, not absolute.

| Regional Trading | MoM Change (%) | YoY Change (%) |

| Asia Hours Price Change MoM ($) | 1 | 2 |

| US hours Price Change MoM ($) | -6 | 1 |

| EU hours Price Change MoM ($) | 0 | 3 |

Source: Glassnode, VanEck research as of 03/17/25. Past performance is no guarantee of future results.

Bitcoin’s Price Action

Market Sentiment

Bitcoin has just experienced its second-largest correction so far this cycle, dropping ~30% peak-to-trough from $109K in January to $76.5K on March 11th, exceed only by a ~33% drop from March 2024 from ~ $74K to ~ $49K in August 2024. While Bitcoin bull markets have historically seen multiple retracements of similar or greater magnitude, this latest decline stands out for contrasting with favorable regulatory developments. Bitcoin ETFs faced their longest outflow streak since inception, losing $6.4 billion over five weeks to Trump’s tariff policies.

Further, broader crypto market sentiment is unusually poor, even for a 30% bull market retracement. Unlike Bitcoin, altcoins have failed to sustain an altcoin bull market, with many already retouching their 2022-2023 bear market lows. This is evident in Bitcoin dominance, which remains mostly unchanged at ~60% this month—a sign that capital is not rotating as aggressively into other crypto assets this cycle as it did in previous cycles.

Bitcoin’s Network Activity, Adoption, and Fees

Transfer Volumes from Miners to Exchanges: With transfers to exchanges down 16% month-over-month, miners are holding onto their BTC treasuries, signaling confidence in Bitcoin’s longer-term outlook.

Daily Inscriptions: Bitcoin inscriptions (mostly “Ordinals”) have grown 62% month-over-month, showing signs of life after an extended cooling off period in Q3 & Q4 of 2024. The Bitcoin NFT ecosystem is showing enthusiasm as Taproot Wizards announced their upcoming mint. The project aims to “make Bitcoin magical again” through initiatives surrounding Bitcoin software developments like OP_CAT, which could bring Ethereum-like smart contract functionality to Bitcoin’s blockchain. Following its $7.5M seed round in November 2023, the project raised $30M in Series A funding this February to build an ecosystem of applications using the OP_CAT Bitcoin improvement proposal.

Bitcoin Futures Annualized Basis: As highlighted in the chart of the month, Bitcoin futures borrowing rates are at their historical 3rd percentile , demonstrating the extent of relative bearishness among traders.

Daily Transactions: Daily transactions grew 9% month-over-month, currently at the 91st percentile of the network’s history.

Total Transfer Volume: Down 5% month-over-month, USD-denominated transfer volumes remain at a healthy 87th percentile of the network’s history. This sustained volume may reflect Bitcoin’s expanding role in international trade settlements, as discussed in ‘Global Trade’.

Average Transaction Fees: Transaction fees remain low in both USD (-14%) and BTC (-2%) terms, indicating that on-chain activity like Ordinals still have not driven sufficient activity to drive up costs.

Global Power Consumption & Mining Difficulty: Bitcoin’s steadily growing global power consumption ticked up 1% this month, remaining at the 100th percentile of the metric’s history as miners continue to energize new capacity.

Total Crypto Equities Market Cap: Demonstrating high beta to Bitcoin, crypto equities dropped 19% this month as markets responded to tariffs and crypto selloffs.

Regulatory and Geopolitical Developments

Despite this month’s price correction, Bitcoin’s macro narrative continues to strengthen, with governments, institutions, and emerging markets making strategic moves into digital assets. Key developments across U.S. regulation, international trade, and corporate adoption suggest that Bitcoin’s role in global markets is expanding.

Washington’s Crypto Reset

In a landmark policy move on March 6th, Donald Trump officially established the Strategic Bitcoin Reserve and U.S. Digital Asset Stockpile , using Bitcoin and other digital assets previously obtained from criminal and civil asset forfeiture proceedings. The administration’s decision to hold, rather than auction, seized Bitcoin signals a fundamental shift in how the U.S. government views BTC—as a strategic asset rather than just confiscated property. While the government has historically liquidated seized BTC through public auctions, this policy pivot suggests that the U.S. recognizes Bitcoin’s role as a reserve asset alongside gold and foreign currency reserves.

The White House is weighing further Bitcoin accumulation for the Reserve. Reports from a closed-door roundtable hosted by the Bitcoin Policy Institute suggest that the White House is considering direct Bitcoin accumulation as part of a broader Strategic Bitcoin Reserve and U.S. Digital Asset Stockpile initiative. According to multiple attendees, Bo Hines, Executive Director of the Presidential Working Group on Digital Assets, stated that any such purchases would be made in a “budget-neutral way that doesn’t cost taxpayers a dime.” This would mark a major shift in U.S. policy if confirmed, solidifying Bitcoin’s position as a government store of value and adding to its list of similarities to gold.

Echoing the Bitcoin Policy Institute’s roundtable, Senator Cynthia Lummis reintroduced legislation aimed at establishing a Strategic Bitcoin Reserve , which would rely on diversifying existing funds from reserve banks and the Fed’s gold certificates. Separately, the Senate Banking Committee advanced the GENIUS Act —a bill with bipartisan support that would create a regulatory framework for stablecoins—as a potential precursor to broader digital asset legislation.

On the enforcement front, the SEC has officially dropped charges against major crypto exchanges including Coinbase, Cumberland DRW, and Robinhood, signaling the end of its aggressive enforcement campaign against the industry. This regulatory shift and the emergence of Bitcoin-focused policy initiatives suggest that Washington’s "war on crypto" is over for now.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。